Making Waves: The Future of Water Innovation — Webinar Highlights

We recently hosted the “Making Waves: The Future of Water Innovation” webinar, featuring insights from Sunena Gupta and Parker Bovée of Cleantech Group, Steve Kloos, Partner at Burnt Island Ventures (a water-focused venture capital firm), and Devesh Bharadwaj, CEO of Pani (a water technology company).

The discussion dove deep into the dynamic world of water and wastewater technology, revealing exciting trends, pressing challenges, and significant opportunities for innovation and investment. Topics covered included venture capital resilience, key technological areas like portable water, AI-powered solutions, and next-generation wastewater systems, and the challenges and opportunities within aging water infrastructure, including the emergence of issues like PFAS.

They also touch upon the investor perspective on the sector and the unique landscape for water innovation in Chicago. The conversation highlights the importance of addressing critical pain points for utilities and industrial users to accelerate the adoption of new water technologies.

VC Investment Shows Resilience in Water Tech

Despite broader economic headwinds, venture capital investments in water technologies have shown remarkable resilience and evolution over the past five years. 2022 was a standout year, with VC investments approaching $750M, nearly double the figures from 2020 and 2021. While there was some comparative cooling in 2023 and 2024, investments remain strong, reflecting a shift towards specific technologies. Early-stage deal activity is still visible, particularly in the monitoring and analytics spaces.

Key Trends Shaping Water Innovation

There are three key trends driving where investment is flowing, offering a glimpse into the future of water innovation:

- Potable Water Innovation: This area consistently attracts major funding, especially for decentralized and energy-efficient purification solutions. Innovators like Gradiant Water are developing full-service industrial water platforms. Source Global creates off-grid hydro panels that harvest clean drinking water from the air.

_

Companies like Adionics and ZwitterCo are working on membrane-free and pre-treatment solutions aimed at lowering the cost and energy demand of desalination. The overarching theme here is a move towards self-reliant and grid-independent clean water tech, crucial given climate instability and infrastructure gaps.

_ - AI-Powered and Sensor-Driven Solutions: There is significant momentum in developing intelligent infrastructure. Companies such as Wint and Leakmited are leveraging machine learning to detect leaks, predict failures, and automate water efficiency across buildings, municipalities, and industries. This trend signifies a shift from just physical infrastructure to smarter, more connected systems.

_ - NextGen Wastewater Systems: Beyond mere compliance, VC funding is increasingly supporting wastewater systems focused on reuse, energy recovery, chemical extraction, and tackling difficult contaminants. Start-ups like Oxyle and Puraffinity are making traction by using advanced oxidation technologies to address hard-to-remove contaminants like PFAS. The focus on PFAS is gaining significant regulatory urgency.

The Pressing Challenge of Aging Wastewater Infrastructure

While innovation is thriving across water technologies, municipal wastewater infrastructure remains particularly under-addressed. Public infrastructure is in a critical state, and these issues need to be tackled at city, state, and federal levels “pretty quickly”. A tangible example is the decaying infrastructure in relation to utility rates. Consumers are now shouldering the cost of looming infrastructure overhauls, with utility rates increasing by approximately 86% over the last decade.

Wastewater utilities see taxpayers as their most consistent funding source, more so than public grants. However, a major issue is a budgetary shortfall, estimated at $69B for infrastructure repairs by the American Society for Civil Engineers. This means infrastructure is being replaced at a rate about 33% slower than 10 years ago. This slower replacement, coupled with massive shortfalls and the age of systems approaching their end-of-life, creates a “counterwave” threatening to have a “crippling effect” on infrastructure. With limited options, utilities are compelled to raise rates, passing the burden to ratepayers.

Innovators Finding Opportunities in the Gaps

Despite these challenges, growth and dynamism are evident in the water ecosystem, from infrastructure tech to digitalization. Innovators are finding opportunities within these infrastructure gaps and inefficiencies.

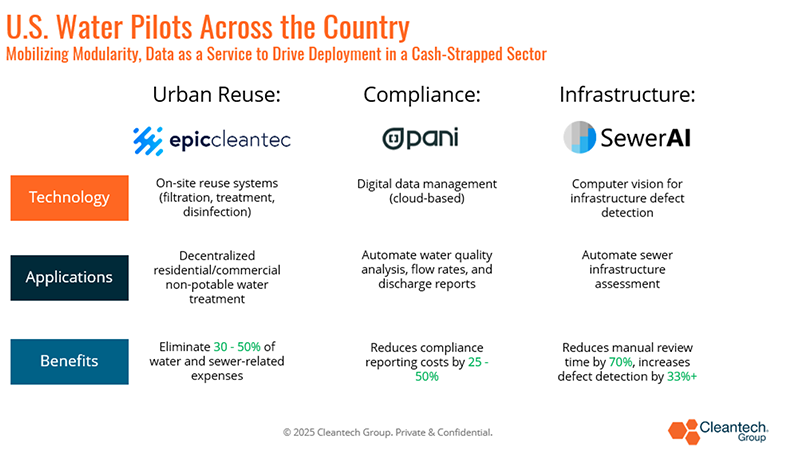

Decentralization of wastewater treatment, both residential and commercial, is one avenue. Epic Cleantec offers on-site reuse systems, like the one at the Salesforce Tower in San Francisco, which provide decentralized non-potable water retreatment. This approach aims to eliminate 30-50% of water- and sewer-related expenses, saving hundreds of thousands of dollars annually.

Software is also restructuring efficiency. Pani, led by CEO Devesh Bharadwaj, is a prime example. Pani leverages “operations intelligence technology” that sits above existing SCADA systems in treatment facilities. These plants, often with complex chemical and biological processes, lack sufficient instrumentation, leading to manual sampling and “firefighting” by operators just to maintain uptime. This is where Pani steps in, filling the gap where critical decisions about servicing assets, detecting issues, and optimizing operations are typically made manually.

Pani offers optimization and compliance reporting for both public utilities and industrial clients, who face complex processes, high compliance needs, and increasing water stress and costs. By improving OpEx and performance, Pani directly impacts yield, water losses, and even greenhouse gas emissions. Pani aims to secure 100 trillion liters of water and reduce 0.1% of global emissions by 2032.

Pani’s impact is seen in real-world examples:

- A municipal wastewater facility in Washington state achieved cost savings, detected issues early (reducing sludge handling costs), and prevented non-compliance. The platform also serves as a valuable tool for retaining “tribal knowledge” as senior staff retire, reducing training time for new operators from months to weeks.

_ - A facility in the Middle East, already well-run, used Pani’s software to reduce its water usage ratio by up to 5% and save costs on downtime, membranes, and chemistry.

Pani sees significant traction in regions like the U.S., parts of Latin America, the Middle East, and India, driven by the combination of industrial sectors and utility needs related to water scarcity and compliance.

Another groundbreaking innovator highlighted is SewerAI. Using compute vision, they automate defect detection in sewer pipes by stitching together camera images. This process is already faster and cheaper than human detection, reducing manual review time by 70% and increasing defect detection by 33% based on human standards. Their work in Houston, Texas, is helping to modernize the city’s infrastructure.

The Investor Perspective: Water is Getting Harder to Ignore

Steve Kloos of Burnt Island Ventures provided the investor viewpoint. Burnt Island Ventures is a specialist firm focused solely on the global water sector. Steve emphasized that the water sector is “pretty huge and underappreciated,” valued at around $1.5 to $1.6 trillion globally and underpinning about 60% of the global economy through its use in agriculture, commercial buildings, and more.

Major forces, particularly climate change, are causing “havoc” by altering the hydrological cycle, leading to more severe droughts and extreme rain events/floods. These changes stress industry, utilities, and the insurance sector. Despite this, water companies and stocks have shown resilience to global economic shifts like tariffs because water is a relatively local issue that still needs to be supplied.

Burnt Island Ventures’ thesis is built on the growing demand for innovative solutions (driven by legacy infrastructure issues) and the increasing supply of talented entrepreneurs entering the water sector, often from outside the traditional industry. Burnt Island Ventures is the most active investor in the water sector, with approximately 29 investments in under five years.

When evaluating start-ups, Burnt Island Ventures looks for “founder market fit,” where founders have unique insights into the problems or solutions, seen as a precursor to product market fit. They also assess the entrepreneurial process, favoring founders who are focused on solving customer problems and creating value, not just those enamored with their technology. Founders need to be agile and capable of navigating challenges from early stage through growth.

Investor interest has grown significantly in the last five years because water issues are becoming “more acute” and “better recognized”. The drivers include climate change impacts, growing pollution concerns like PFAS, microplastics, and nutrients, and the undeniable reality of aging infrastructure. With 800,000 miles of sewer pipes in the U.S. and 1.5 million in Europe, many installed post-WWII with a 50–70-year life, the end-of-life is here. Compounding this, governments are deeper in debt, meaning the money isn’t available for traditional “dig it all up and replace them all” solutions. Shockingly, about 30% of treated drinking water in the U.S. is lost through pipe leaks. These acute problems necessitate innovative solutions.

Utilities and Risk Aversion: Navigating the Path to Adoption

A common perception is that utilities are risk-averse and slow to adopt new technologies. Devesh Bharadwaj explained that getting traction involves identifying the utility’s “true pain,” understanding the specific people facing that pain, and providing evidence through case studies from similar utilities. The pain relief offered by the solution must be significant enough to outweigh the perceived risk and change management involved. Starting small, often through pilots, helps build trust, and leveraging testimonials from other utilities is key.

Steve Kloos offered a counterpoint, arguing that utilities are not always slow, particularly when it comes to digital solutions. Companies offering digital improvements like Sewer AI, Daupler, and Ziptility can see relatively short sales cycles (less than 90 days) because utilities have processes “stuck in the 80s and 90s” and are open to help for their large problems. The key distinction is the perceived risk: enhancing what a plant is already doing with a digital solution involves low perceived risk compared to major retrofits. For more capital-intensive solutions, gaining reference cases in the industrial sector first is a recommended strategy before approaching utilities.

Looking Ahead: Needed Breakthroughs in Water

The panel shared their perspectives on needed breakthroughs:

- Devesh Bharadwaj highlighted the need for more clarity and objective frameworks for treatment facilities to understand and benchmark their performance. This would help them identify gaps and accelerate investments in improvements. He also called for seamless, simple, and cheap instrumentation for treatment facilities, noting that installation processes still need significant improvement. These two breakthroughs, combined, could accelerate the transformation rate of these assets.

_ - Steve Kloos pointed to the urgent need for transformation in biosolids (sludge) treatment. Biosolids, a byproduct of wastewater treatment containing solids and excess biomass, are typically dewatered and sent to landfill or land application. However, the presence of microplastics and increasingly, PFAS, in sludge is causing significant issues. Farmers are suing over PFAS contamination when sludge is used as fertilizer, forcing utilities to re-evaluate disposal methods. Moving completely away from land application to better treatment methods is a critical upcoming challenge.

Conclusion

The water sector is facing unprecedented challenges driven by climate change, aging infrastructure, and evolving contaminants. Yet, this is also fueling a wave of innovation and investment. From decentralized water solutions and AI-powered systems to next-generation wastewater treatment and novel approaches to utility adoption, the future of water technology is ripe with opportunity. Collaboration among innovators, investors, and utilities, like the “Burnham spirit” seen in the Chicago region, will be essential to navigate this evolving landscape and build a more resilient and sustainable blue economy.