Curated Capital in a Risk-Filled World: Cleantech’s Mid-Year Funding Reality

An unpredictable H1 2025 has shaped new needs for the innovation ecosystem for more carefully curated funding that can withstand potential shocks to the funding landscape. We took stock of some important themes in the past six months:

- The desire for energy security informed technologies that receive funding with market leaders adopting increasingly protectionist attitudes to combat uncertainty and geopolitical dynamics. Countries are veering away from higher risk energy tech (i.e., solar PV production), with geothermal and hydrogen technology receiving some support, albeit at lower levels than previous quarters.

_ - Infrastructure-focused purposes behind funding rounds: To meet rising demand, there’s been an increased emphasis on building out and strengthening existing infrastructure, with particular emphasis on grid technologies and manufacturing.

_ - Expanding opportunities in and around AI influenced cleantech development: AI remains a significant influence on which sectors keep netting equity funding. Energy efficient computing, sustainable power sources for data centers, and technologies that strengthen AI’s compatibility with existing energy and grid infrastructure and its applications in food security, transportation, and manufacturing are areas of growth.

As we move into H2, let’s check in on some predictions we made earlier:

Less is More (Literally)

Prediction: Larger, more deliberate funding rounds will continue to govern the movements of the cleantech ecosystem, carrying on funding trends established late last year.

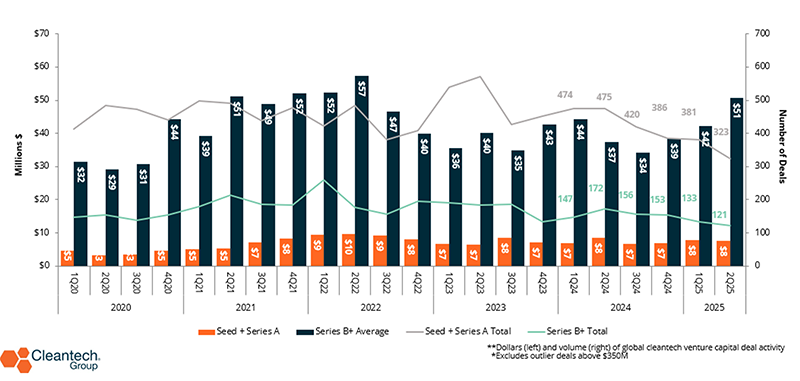

Were we on the money? Looks like we were, as this funding attitude was very visible in the first half of 2025, having been established at the end of last year. Later-stage ticket sizes have increased on average by 35%. Early-stage deals are smaller and less frequent overall.

Cleantech Funding by Stage: 2020 – 2Q 2025

The mid-stage funding ‘valley of death’ continues to widen for start-ups at the Series A stage as innovators take longer year-on-year to raise further funding. Rising energy costs, exacerbated by shifts in U.S. policy towards coal-powered ‘American energy dominance’, threaten the viability of cleantech development that relies heavily on material exports and global supply chains:

- While early-stage activity in APAC has been on a steady decline since 2024, substantial investment in tried-and-tested sectors like energy efficient heating, ventilation, and cooling (HVAC), sustainable logistics, and smart livestock management drove up average late-stage round size by 49% in H1 2025 from H2 2024.

_ - The February release of the EU’s Omnibus simplifying sustainability reporting and disclosure supported regional interest in environmental monitoring. Funding peaked in Q1 through early-stage deals, then helped to bump Q2’s average late-stage round sizes through spacecraft designed for aerial monitoring and earth observation. Space-related tech with applications in environmental monitoring gained traction in 2025, helped by EU-wide initiatives like the European Space Agency’s EU Space Act aimed at strengthening regional space-related technology development and deployment.

_ - Sustainable mining innovations nudged up early-stage activity in North America. Recent efforts by the Carbon Alliance push to tie mining policy with carbon capture, with the latter being one of the few cleantech sectors that is continuing to receive grant funding into this year. Bilateral efforts between Canada and Mexico promoting sustainable mineral resource governance supported some late-stage investment into AI-powered extraction/surveying technology.

Cog in the Machine

Prediction: Commercial/corporate engagement will increase in a ‘thinner’ investment environment.

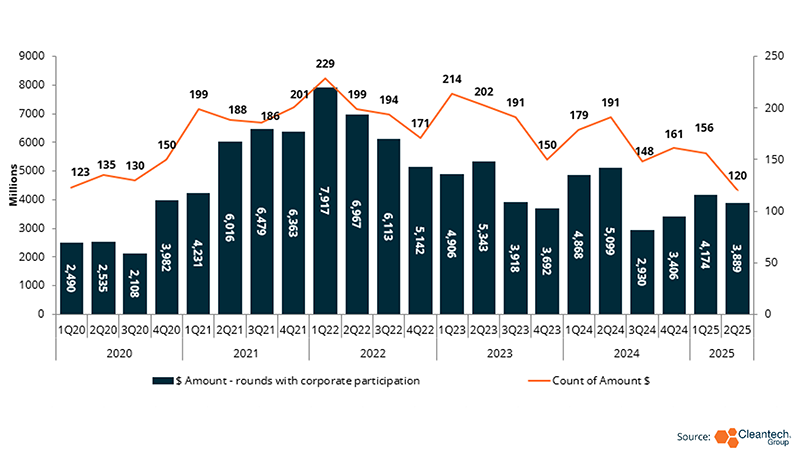

Were we on the money? Corporate participation in venture investment seems to have slowed down with the number of deals with corporate participation falling by 9% from H2 2024 to H1 2025. Overall private investor participation decreased by 20%. H1’ s venture-backed mergers and acquisitions (M&A) add nuance to this slowdown, having maintained relatively steady levels since 2023. Q2 of this year saw M&A activity center around energy networks and grid innovation, helmed by NRG Energy’s $12B acquisition of CPower aimed at increasing presence and production.

Corporate Participation in Cleantech Funding: 2020 – 2Q 2025

Tipping the Scale

Prediction: The surge of first-of-a-kind (FOAK) technologies hitting the market and raising funding in 2024 will signal stronger emphasis on scaling overall.

Were we on the money? This year’s venture rounds worked towards increasing production, furthering product and technology deployment, and working towards realizing infrastructure able to cope with growing energy demand. An ecosystem-wide desire for security, namely energy security, informed decision-making and capital flow across all regions.

Energy storage, nuclear, and sustainable fuel-related FOAK projects and facilities received significant equity funding in Q2 2025. Hybrid debt/equity or debt/grant packages will support the construction of FOAKs for renewables production in Europe and the U.S. to be deployed in the next 3-4 years. Conversely, large-scale solar and battery manufacturing projects were cancelled having been affected by targeted policy changes and rising costs.

- European ecosystems aligned their efforts with cleantech-related infrastructure development, focusing on addressing regulatory challenges that prevent large-scale deployment for sectors like electric vehicle charging.

_ - Regional governments in Canada heighten focus on critical materials: Ontario’s proposed Bill C-5 would streamline major infrastructure reform by quickening the authorization process. This could encourage local investors to support innovators decarbonizing infrastructure reform that may need such projects to scale up.

_ - Latin America has produced compelling FOAK projects and technologies in the last six months, including Niko’s first virtual power plant in Mexico and Atome PLC’s ammonia-based fertilizer production facility in Paraguay, scaling solutions that work towards long-term energy and food security.

Playing the Long Game

H1 2025 has shown that investors haven’t lost their appetite but are looking to optimize their capital in a risk-filled environment. Opportunities with demonstrated profitability or multiple use cases are likely to withstand further potential shocks to a rapidly evolving landscape. Alongside security, resiliency will help define the attitudes of investors and ecosystem actors through H2 2025:

- Corporates will find some opportunities in M&As for energy tech innovators that target increased demand for energy security, brought about by the acceleration in AI and data center development.

_ - With a volatile public-funding environment, innovators at earlier development stages will need more consistent support from the private sector to develop their technologies to a scalable product. Start-up incubators (academic and private) are well equipped to fill and take advantage of this gap.

_ - Strategic, innovation-focused partnerships will be key for innovators at all stages, from acceleration to commercialization.