Ammonia for Maritime Decarbonization

Ammonia is currently one of the most divisive topics in the maritime decarbonization space. The decarbonization potential of ammonia is undeniable: ammonia (NH3) does not contain carbon, meaning it eliminates CO2 emissions at the point of combustion, and is an ideal hydrogen carrier.

Due to these climate-positive characteristics as well as the extensive existing shipping and handling network and high potential for production scalability, an increasing number of shipping and maritime actors are basing their decarbonization plans around ammonia. The view that ammonia is a panacea for maritime decarbonization challenges is far from ubiquitous across the maritime industry, however.

Orderbook for Alternative Fuel Vessels (May 2024)

Skeptics point to practical and safety challenges that must be overcome for the widespread uptake of ammonia as a maritime fuel: namely, non-CO2 emissions from combustion (NOx, N2O), methane slip, and the serious human and environmental hazard posed by methane spills. Even for those fleet owners and operators undeterred by the potential safety risks, ammonia faces the same chicken-and-egg challenge of all zero- and low-emissions fuels: fleet operators will not commit to adapting fleets for ammonia without a clear supply of green ammonia, while potential green ammonia suppliers cannot invest in production capacity without a strong and committed demand signal from users.

As the maritime sector grapples with this vicious circle, several global players (e.g., Fortescue, Yara, MOL, CMB.Tech), are attempting to simultaneously drive production while supporting the development of the demand market and supporting infrastructure such as bunkering and storage facilities.

Innovation: Technology Addressing Pain Points Along the Ammonia Value Chain

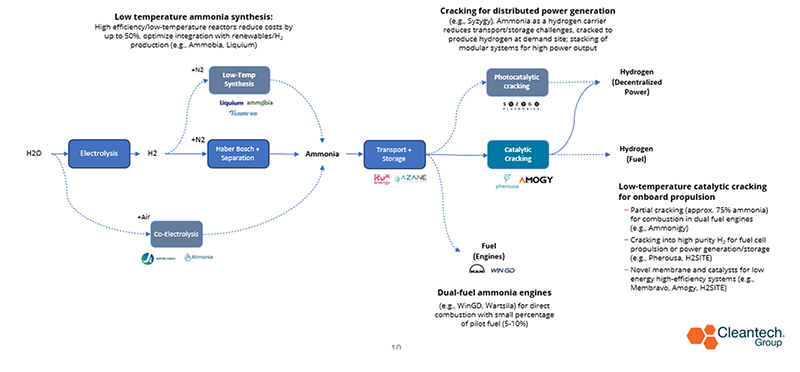

- Ammonia synthesis: Innovators developing low-temperature, higher efficiency synthesis processes to reduce fuel costs and facilitate integration of renewables

__ - Ammonia engines: Conventional ICE engines must be adapted to combust ammonia. Several OEMs are close to commercialization of dual-fuel ammonia and conventional fuel engines, enabling fuel flexibility and reaching up to 95% CO2 emissions reductions. Additional systems must address NOx/N2O emissions.

_ - Ammonia cracking: Leveraging ammonia as a hydrogen carrier, innovators are adapting conventional, high-temperature ammonia cracking (splitting ammonia into hydrogen and nitrogen) to power vessels and stationary generators with green hydrogen:

_- Low-temperature catalytic cracking systems for onboard propulsion, combined with hydrogen combustion, or fuel cells (e.g., Amogy, Ammonigy, Pherousa)

_ - Novel membrane reactors for efficient hydrogen separation and purification (e.g., Membravo, H2SITE)

_ - Ammonia cracking can be situated at ports to provide clean hydrogen to electrify equipment and vessels, as well as onsite energy storage

- Low-temperature catalytic cracking systems for onboard propulsion, combined with hydrogen combustion, or fuel cells (e.g., Amogy, Ammonigy, Pherousa)

Key Innovations Unlocking Decarbonization Potential of Ammonia for Vessels and Ports

Ammonia cracking in itself is not a novel technology, but conventional systems are not suitable for vessel propulsion or distributed power generation. Crackers operate at high temperatures (up to 900°C), have large physical footprints, and massive energy demands. Innovators and innovative corporates are adapting conventional crackers in several ways to meet the specific demands of both the maritime and power generation sectors.

KBR, developer of hydrogen and ammonia production solutions, is leveraging existing components and infrastructure to deploy large-scale ammonia cracking systems. Targeting 10-1,200 tonnes per day of hydrogen, KBR´s thermal catalytic process leverages a nickel-based reactor and reports a hydrogen yield of 80% (with remaining 20 units reutilized as a clean fuel source) or up to 96% if powered by natural gas.

While currently engaging with the power generation sector, KBR has identified the maritime fuels sector as a key demand market for ammonia in the coming years, outpacing even the demand from the fertilizer industry (currently 80% of global ammonia demand).

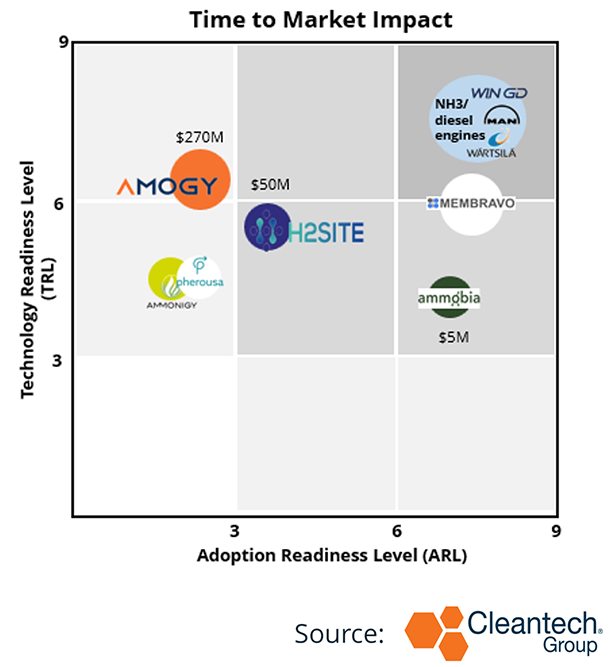

Projections for Future Clean Ammonia Demand (2045): Start-up Landscape: Ammonia Cracking for Vessel Propulsion

Ammonia Maritime Solutions Landscape

A core group of start-ups are developing bespoke, modular ammonia cracking solutions for vessel propulsion and onboard power. Innovators combine proprietary system and catalyst design with “power-packs” and vessel engine room redesign to develop zero-emissions vessels. Key differentiation points include hydrogen separation efficiency and purity, integration into propulsion systems (e.g., turbines, fuel cell), and overall energy and system efficiency.

While component technology is mature (TRL 8-9), novel vessel designs must undergo a rigorous testing and certification process before start-ups can embark on pilots and demonstration projects. Securing onboard pilots is a key obstacle for innovators to overcome in order to provide real-world data and improve market acceptance of ammonia technologies.

Looking forward…

- Development of ammonia production and bunkering infrastructure is essential to support widespread uptake of ammonia as a maritime fuel

- First solution to market will be dual-fuel ammonia engines: deployment of ammonia-compatible vessels will bolster infrastructure deployment, while vertically integrated corporations must continue to drive both demand and supply of ammonia

- Ammonia cracking innovators will benefit from increasing market familiarity with ammonia, facilitating larger-scale demonstrations and technology advancement to address emissions, bring down costs, and improve efficiency

- Innovators and incumbents must carefully identify chosen target markets, but market conditions (cost of green hydrogen, de-globalization of energy sector, maritime carbon penalties) are determining factors in cost-efficiency of ammonia as a fuel and as a hydrogen carrier for power generation