Flexibility: Window is Closing for New Innovators

The world needs more flexibility. Renewable electricity additions across the world are breaking records but balancing this new supply is becoming a major headache for system operators. The intermittency of renewables is creating problems with maintaining the grid frequency – set at 56-605HTz in most Western countries – and inertia. Meanwhile building new grid infrastructure is nigh impossible due to access to land restrictions and supply chain bottlenecks. New load centers, such as electric vehicles and heat pumps, add further stress to the grid.

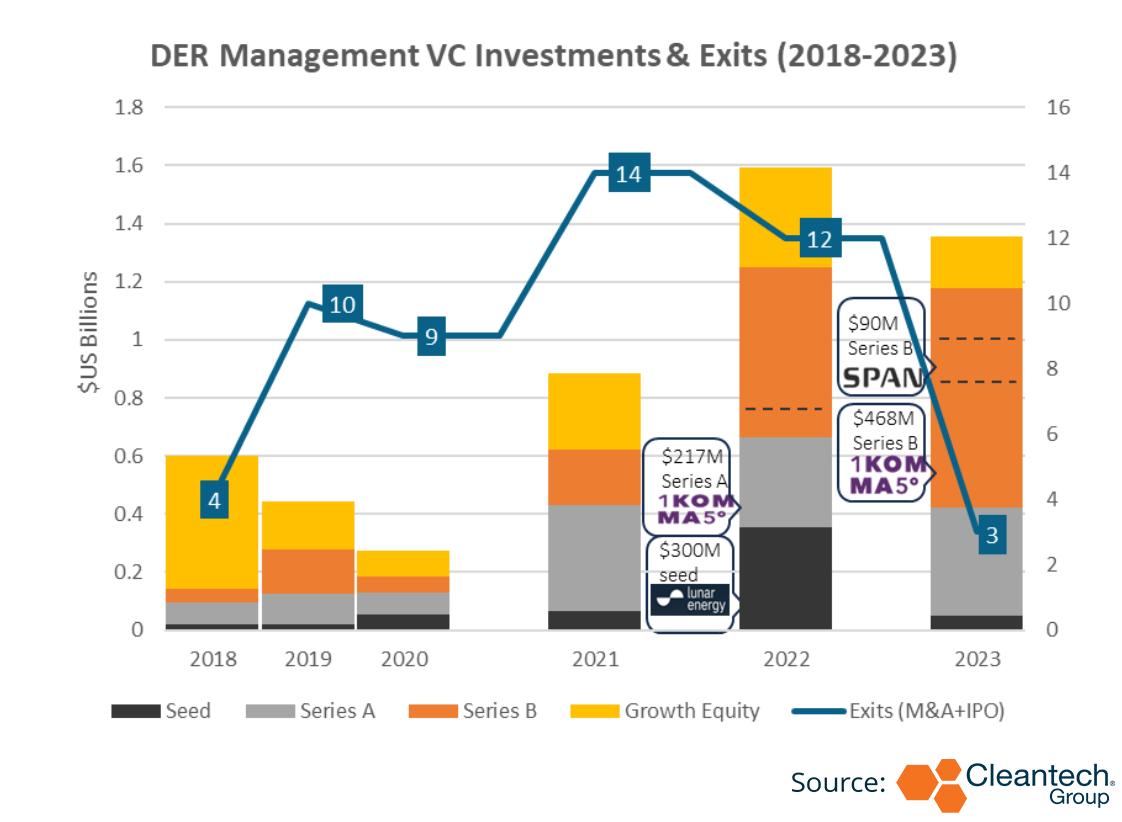

Despite an increasing need for flexibility, innovation is stalling as software providers have been able to leapfrog the regulation. Venture and growth investment numbers show that flexibility-related investments have plummeted in 2023, with just $338M invested. The number of exits and initial public offerings (IPOs) have also plummeted, and exiting is not as easy as it used to be – Shell has been looking for buyers for Sonnen, a smart energy storage and virtual power plant it purchased only in 2019, since September 2023. A number of venture capital providers in primary interviews with Cleantech Group have said that they are currently pulling back from the flexibility space.

This is a far cry from just a few years ago. Over 2021 and 2022, Cleantech Group tracked a record amount of $1.48B of investment into distributed energy management solutions. These included supply and demand aggregation and more. As interest rates surged in 2022, digital technologies were a low hanging fruit for venture capital, made attractive by low required CAPEX to scale technology and therefore lower risk, “as-a-service” models locking customers in, as well as easier routes for exits. Companies like demand response aggregator Voltus raised $31M in growth equity, while VPP and DER aggregator AutoGrid raised $85M in growth equity. Demand for asset light high return software solutions was soaring.

There has been a clear pivot away from DER management software investments towards more hardware-heavy integrated providers. Even established players, such as local flexibility marketplace Piclo and marketplace Leap have raised relatively small rounds in 2023. Leap raised $14M in two Series B rounds, while Piclo raised $10M in a Series B round.

In comparison, intelligent home hardware provider Lunar Energy came out of stealth in 2023 and raised $300M in a Seed round. One-stop-shops, companies that integrate both software and hardware and sell a bundle of solar PV, storage, and energy management systems, like 1Komma5, Span and Lunar can also provide flexibility but that is not their main business model.

Having said that, the need for more flexibility is still very pertinent. The distribution system operators in the UK say they are only ever able to secure up to 50% of the flexibility they need in any particular locality.

Software Moves Fast, Policy Moves Slow

A good example is the FERC 2222 mandate. Despite the FERC ruling for member states to facilitate more DER in grid management, only a few states have made tangible progress. The picture in Europe is also mixed. UK grid operators and the regulator have made great efforts to integrate DER into the energy management picture including contracting flexibility on the local level. On mainland Europe, only a handful of countries allow for DER participation in grid flexibility, mostly because the transmission system operators operate under a CAPEX not TOTEX regime and so are mostly focused on making capital investments to get returns.

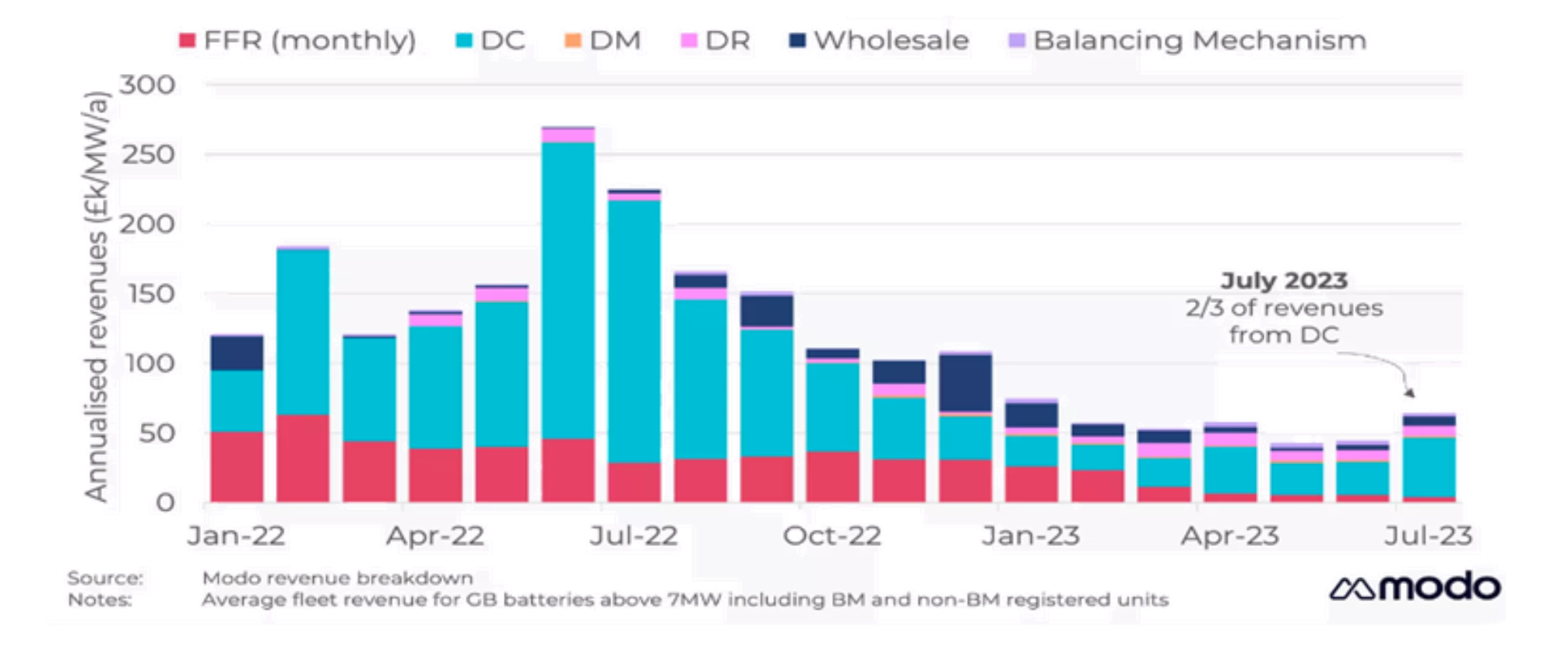

In geographies where flexibility is allowed, it is already making a tangible difference. In December 2023, the 2GW IFA power line between France and the UK tripped and lost half of its output. In response, a UK utility, Octopus, was able to mobilise 400MW of batteries to offset some of the outage. Over the winter period in 2022, the UK was able to call on 4GW of flexible resources.

Distributed battery assets have also been instrumental in maintaining grid stability in a number of European countries through to the frequency containment reserve (FCR) instrument that compensates assets that are able to ramp up in sub 30 seconds in the case of an outage. However, in geographies with high battery proliferation, FCR prices are coming down.

Existing innovators are already working with regulators to open up more flexibility in new geographies, making it harder for newcomers to enter the market. Leap worked with California ISO CAISO on the new Demand Side Grid Support (DSGS) to include more battery asset grid services. Piclo already co-operates with four out of six transmission system operators in the UK and is working with TSO’s of Lithuania, Portugal, Italy and Ireland to open up new flexibility in those geographies. Estonian Fusebox is working on a pilot in the Danish market.

Software solutions that do everything that is required to add more supply/demand side flexibility to a transmission or distribution grid in the existing framework already exist. This, coupled with the fact that innovators who have developed this software are actively working with regulators to open up more flexibility, makes it difficult for new providers to enter this very competitive space.

Cleantech Group currently tallies 177 DER management companies in the i3 database. Considering how much headway the incumbents in this space have made and how few markets allow for DER participation in grid management, it is likely that we will see further consolidation. Many of the innovators will have proprietary software that will be attractive for utilities, but for new pureplay DER management companies the window of opportunity is rapidly closing.