Floating Offshore Wind – The Race to Scale

In September 2021 experienced offshore wind developer Ocean Winds ( 950 MW Moray East) and Aker ( offshore construction and services) submitted a bid to ScotWind for 6,000 MW using floating wind turbines. France announced a tender, May 2021, for 230-270 MW floating offshore wind. On the other side of the pond, Oregon put forward a bill to develop 3GW floating offshore wind capacity by 2030, all part of Biden’s efforts to install 30GW of offshore wind by 2030. Korea and Japan are also committing to large offshore wind projects.

These sizeable commitments are signs of the evolution of offshore wind innovators and the need to scale projects to further reduce levelized cost of energy below that of fixed foundation projects.

Is it really needed?

A staggering 80% of the world’s offshore wind resource potential is in waters deeper than 60 metres, with high probabilities of consistent, high-speed wind and relatively close to demand centres. The opportunity is especially prevalent for nations residing next to deep water shelfs, such as west coast US, Korea and Japan

Over the past decade, floating wind has gone through a rigorous period of testing. Now the market is ready to undergo a substantial scale-up, with industrialization, standardization, permitting top of mind and for floater technology innovation to go through a rigorous period of consolidation in the coming years.

Technology to match offshore project requirements

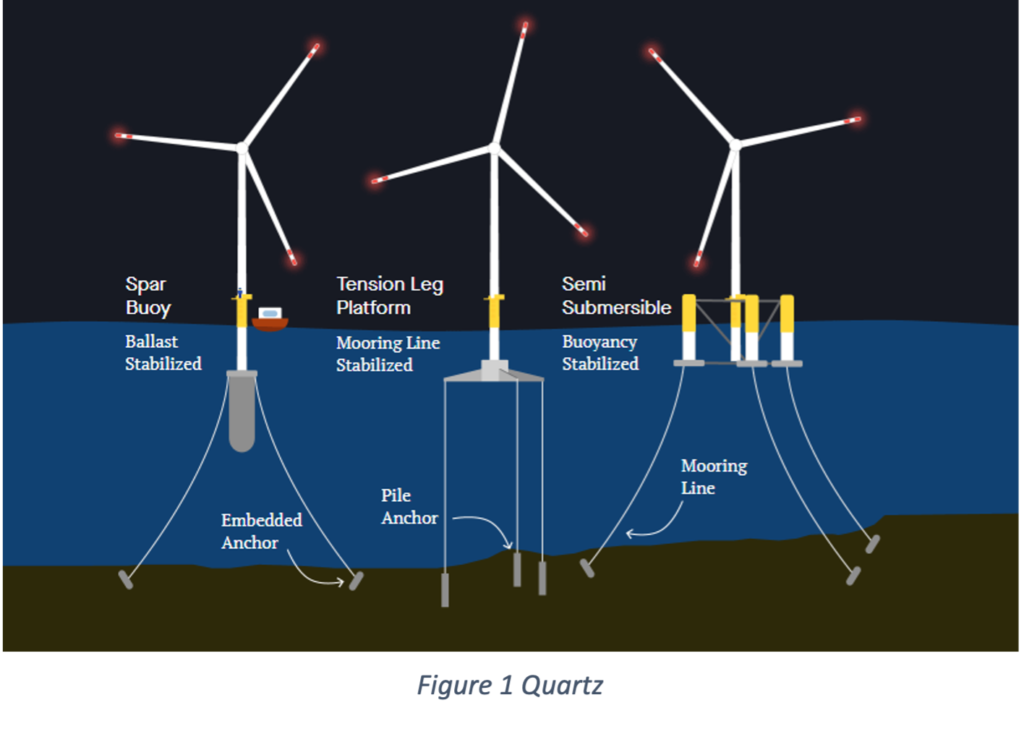

For floating wind, innovation is focused on the design of a floating structure platform to support one, or even multiple turbines under extreme conditions, while reducing cost of installation. While there have been well over 50 variations of floater technologies cited in testing, three designs have benefited from further testing and development time through pilots/small-scale demonstrations and thus are now leading the transition towards large-scale commercial projects. The designs, Spar Buoy, Tension Leg and Semi-Submersible, have also seen various hybrid options tested. These designs are highlighted in figure 1.

For systems to be selected by a project developer, various characteristics of a project are considered, including:

- Water depth suitability

- Wind turbine size requirements and ability to support bigger systems

- Ability to be manufactured at scale and ability to be quickly set-up without expensive towing logistics

- Material requirements, and the overall embedded carbon, contribution to project additionality

- Post-procurement service options, including maintenance end-of-life support

- Most importantly, overall energy yield potential

Designing a business model to suit rapid scale-up

France-based BW Ideol, founded in 2010, developed a semi-submersible floating system, offering the solution as a co-developer and engineering service provider with longer term goal to also operate plants. Targeting 30+ meters depth, with a promise of 50% relative cost savings, the company is also looking to differentiate by, offering a flexible system which is buildable in steel or concrete with variations on construction. At the start of this year, the company merged with BW Offshore before listing onto the Euronext Growth Oslo to support a transition from pre-commercial projects to 10GW capacity by 2030.

Sweden-based Hexicon, a semi-submersible tension leg floater provider, founded in 2009 also went public in June 2021, Nasdaq First North. Their system which offers the ability to host two wind turbines on single platform also offer development services, where the team do permitting, put in capital, find development partners, as well is identifying EPC and operation.

Another well-funded innovator in the space, Principle Power, founded in 2007, offers a 3 column semi-submersible system, as well as maintenance services. With 75MW capacity, the company are industrializing by 2023, aiming for 15GW by 2030. Principle Power has been equity funded by offshore developers and energy majors including Aker Solutions, EDP, and Repsol, who are licensing the floating system

Earlier stage innovators, including Gazelle Wind Power, Ocergy and X1 Wind are focusing initially on traditional technology licensing as routes to market.

Corporates are repositioning alongside technology providers

Infrastructure asset investors/mangers, offshore project developers and oil & gas majors see floating wind as a big opportunity to capture a large value of the overall share in long-term renewable energy capacity.

Energy majors including Shell, BP, and Total are heavily investing seeing an opportunity to capitalise on decades of off-shore experience. The former, aims to develop 12GW of offshore wind capacity by 2030, acquired floating offshore developer Eolfi back in 2019, and has partnered with innovators Simply Blue Energy and Stiesdal Offshore for multi-GW projects. Companies such as Macquarie for example, are positioning as platform agnostic project developers, seeing different opportunities for various solutions in different geographies and are active globally.

A pivotal decade

By 2035, 11–25% of all new offshore projects globally will feature floating foundations, but costs between fixed bottom and floating will need to continue narrowing as the pace needed for projects to be bankable for long-term clean energy financers.

Keep an eye on

- Capital: the SPAC market trend could include floating wind next year as technology companies look to rapidly access capital

- Planning: Digital maritime spatial planning to address project uncertainty, planning streamlining and unnecessary costs

- Integration: Innovators broadening floating structure offerings for a boarder range of energy technologies incorporating floating with onsite wave energy generation, integration hydrogen production or energy storage