Green Steel: Innovations Can Enable Cost-Effective Deployment at Scale

Steel production is one of the largest industrial sources of carbon emissions, accounting for up to 10% of global CO2 emissions — and steel isn’t going anywhere with production set to increase up to 2050. This has led to increased pressure from governments, consumers, and investors to reduce emissions and transition to more sustainable production methods.

Recent policy measures such as the $5.8B for Advanced Industrial Facilities Deployment in the U.S., combined with development of more efficient production technologies which can help eradicate the green premium, will accelerate deployment of emissions reduction technologies.

Anthony Vicari and Ian Hayton of Cleantech Group talk about the steps currently being taken to decarbonize steel, and what the future of this industry might look like.

Current Steel Production and Mature Approaches to Mitigation

Most of the steel produced today (around 70%) is made using the blast furnace-basic oxygen furnace (BF-BOF) production route where iron ore is melted in a blast furnace (BF) and then further processed in a basic oxygen furnace (BOF) to remove impurities and add carbon. The process emits around 2 tonnes of CO2e (carbon dioxide equivalent) per tonne of steel produced.

Producers have already adopted steel production technologies which enable a reduction in emissions.

- Scrap recycling is deployed at scale and brings emissions close to zero, but it is constrained by the availability of scrap steel.

- Direct reduction of iron ore using natural gas (NG-DRI) reduces emissions by around 50% compared to the integrated BF-BOF production route and is also deployed at scale with over 100 million tonnes of DRI produced in 2021.

There are also a number of initiatives targeting emissions reduction in the BF-BOF production route including top gas recycling, hydrogen injection or the use of biomass in place of coke. Although these approaches are important to enable the transition of BF-BOF steelmaking facilities, the reduction in emissions will not be sufficient to reach climate goals.

Application of carbon capture and storage can address emissions at a cost, and if the necessary infrastructure is available or can be deployed. Carbon capture and use in fuels/chemicals, as demonstrated by Lanzatech, can displace emissions from fuels/chemicals produced elsewhere.

More recently, the trend for industrial-scale mitigation has shifted towards the use of hydrogen for direct reduction of iron ore (H2-DRI). This process can bring emissions from steel production close to zero, depending on the source of hydrogen. Many incumbent steel producers are deploying H2-DRI production processes including Arcelor Mittal, ThyssenKrupp, SSAB and POSCO. Several start-ups have also raised funds and engaged with technology providers to scale up the H2-DRI production process including H2 Green Steel, GravitHy and Blastr.

The hydrogen direct reduction process benefits from the maturity of technology supplied by Midrex and Tenova, both of which provided direct reduction technology for use with natural gas. There are also a number of technology variants under development which can use low grade ores, or fines. For example, Greeniron has developed hydrogen-based processes which enable the recycling of iron residuals and waste materials. Greeniron raised $11M in 2021 and is building a first plant in Sweden, with operation expected to start later in 2023. Other technology owners in this space include Metso Outotec, Calix, Primetals Technologies and POSCO (steelmaker).

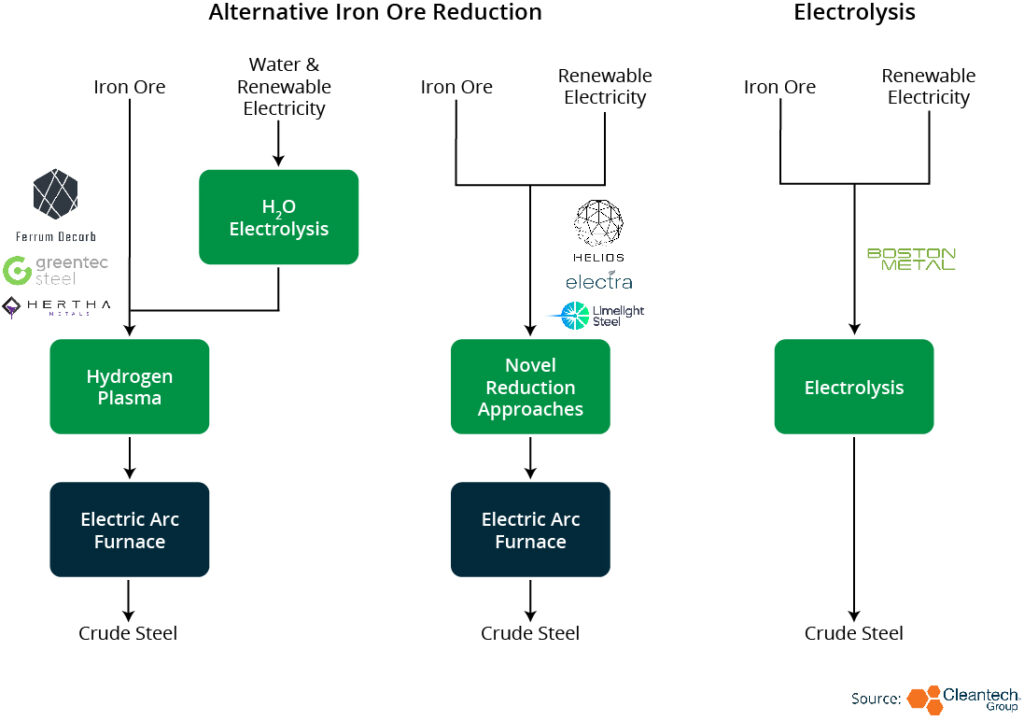

Electrolysis, Hydrogen Plasma and Other Iron Ore Reduction Processes

Touting lower energy usage, greater modularity and/or the potential to use lower-grade iron ores, the past two years have seen strong growth in the development of alternative iron and steelmaking technologies which can reach commercial maturity in the latter half of this decade.

Boston Metal is developing Molten Oxide Electrolysis (MOE) technology which directly produces high-purity molten iron. The technology works with all grades of iron ore and does not require process water, hazardous chemicals, or rare-metal catalysts to operate. Boston Metal raised $120M in the first close of Series C fundraising led by steel producer, ArcelorMittal. The company already operates a pilot plant and expects to be in deployment at demonstration scale by 2024 with commercial availability expected in 2026.

The development of hydrogen plasma smelting reduction has gained traction recently with Hertha Metals developing the technology whilst supported in the Breakthrough Energy Fellows programme. The approach involves the reduction and smelting of iron ore with green hydrogen and green electricity and has the potential to significantly enhance reduction rates, improving efficiency and ultimately lowering costs. Hertha aims to demonstrate a five-ton furnace that produces molten iron through hydrogen and electricity this year and begin deploying steelmaking units that can process 200 thousand tonnes per year to integrate with existing steel mini-mills by 2027.

Similar approaches are also being pursued by Voestalpine, Ferrum Decarb, and Max Planck Institute.

There are also a number of other start-ups pursing different approaches to ironmaking, but sharing similar goals — increased flexibility in terms of feedstocks and/or energy usage and/or reduction in energy usage:

- Electra is developing ‘low temperature ironmaking’ which is based on aqueous electrolysis. Electra raised $85M with backers including Breakthrough Energy and BHP.

- Helios uses sodium as a reducing agent. Regeneration takes place using thermal energy which lowers energy usage. Helios raised $6M in 2022 to fund further development.

- Limelight Steel uses optimized light energy as a heat source, again lowering energy usage. Limelight steel joined the Activate Fellows Program in 2022.

Looking Forward

To ensure successful scale up of these new approaches, several factors need to be considered:

- Policy measures, such as carbon pricing and emissions regulation will be critical in penalising emitters and incentivising emissions reduction.

- Clear market signals such as commitments to procure green steel, including through initiatives such as SteelZero, will demonstrate demand.

- Long term offtake agreements can help to de-risk projects enabling access to finance.

- Large-scale deployment will be dependent on addressing bottlenecks across the value chain, such as the availability of renewable energy and/or low carbon hydrogen, which will need to be addressed. First-of-a-kind plants will benefit from special financing such as Breakthrough Energy Catalyst.

Finally, early-stage technologies remain higher risk and grant funding can help support their development. With appropriate support, new approaches such as CO2 reduction and recycling in blast furnaces or direct use of ammonia as a reductant, could increase the speed and applicability of low carbon steel production.