Let’s Get Critical

Even within our own Cleantech Group, we all have different viewpoints on this sector based on our backgrounds and research focuses. So, we challenged a few with the same Hot or Not activity.

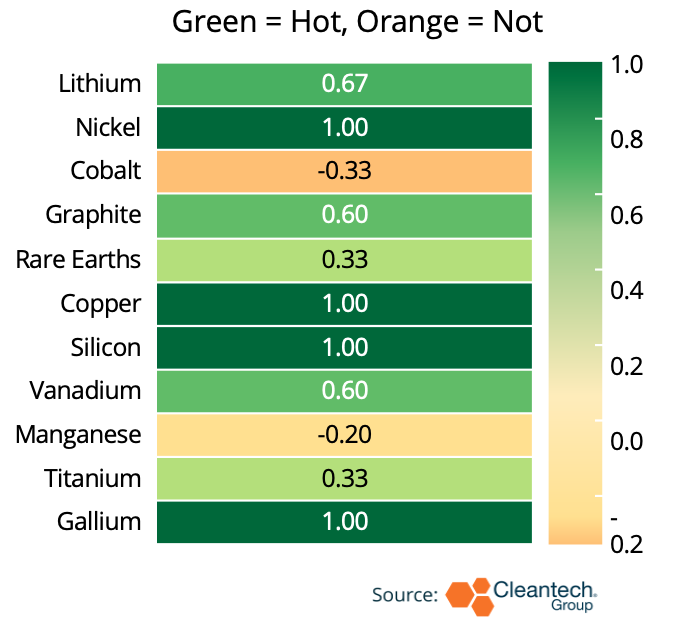

Net Analyst Sentiment Score

Parker Bovee (Waste and Recycling) on Graphite (Not):

“Very similar market compared to lithium, but margins are so bad it may not even make sense to on/nearshore it. There is an argument to be made for still trying to bring it domestic since China controls 90%+ of the entire value chain but it has yet to be valued highly enough to motivate anyone to disrupt this.”

Sunena Gupta (Resources and Environmental Management) on Lithium (Not):

“I think there are potential overpromises on finding new lithium resources.”

Buff Lopez (Materials and Chemicals) on Gallium (Hot):

“The semiconductor is a core component of the digital age, think solar panels, EVs, computers, etc. But the metals required all face severe shortages, especially gallium which is 90% processed and refined in China.”

Zainab Gilani (Energy and Power) on Vanadium (Hot):

“Vanadium’s infinite recyclability and potential for leasing make it a compelling option—particularly in China with its domestic supply chain—but high costs still limit competitiveness with lithium. A hybrid vanadium-lithium storage system could optimize performance by using lithium for rapid response and vanadium for long-duration storage. Additionally, electrolyte leasing models can bring the upfront costs of batteries down and potentially shield customers from the volatility of vanadium prices.”

Diana Rasner (Group Lead) on Rare Earths (Hot):

“There aren’t mines for rare earths the same way you’d think of things like iron, copper, or tin. They’re literally everywhere (ironic considering it’s called “rare”) in all sorts of different ores and rock within the earth’s crust, just at low concentrations.

The ability to get to them, let alone process and refine them, makes rare earth production a matter of scale and further precision to separate, leads to their high costs. Digitization, the clean energy transition, our modern-day luxuries of electronics and LCD screens are not possible without rare earths and we’re only going to need more of them as time goes on.”