Methane and Climate Mitigation: Outlook for Innovation and Progress

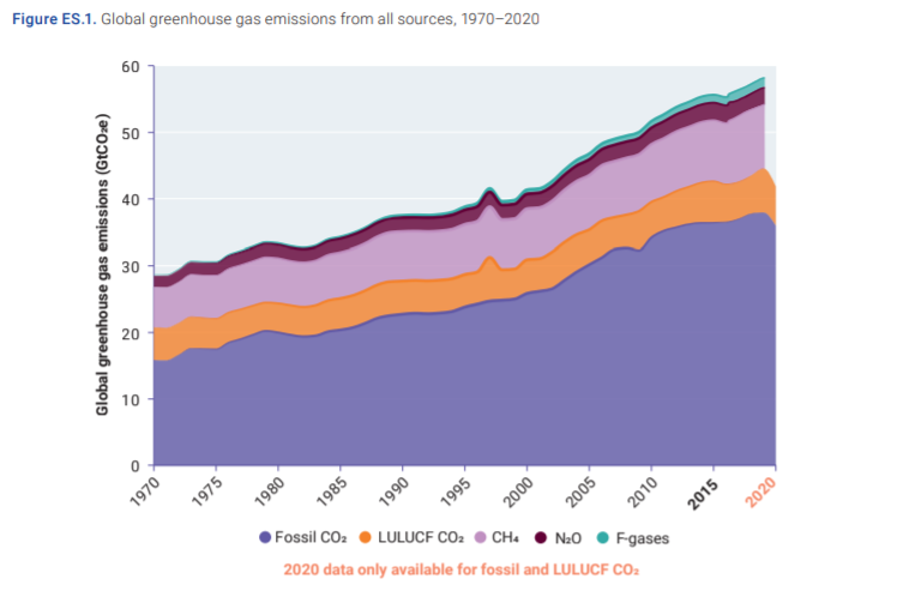

Methane has a global warming potential 86 and 28 times higher than CO2, over 20 and 100 years and is responsible for 23% of all global warming. Around 60% of methane emissions originate from anthropogenic sources including landfills, livestock raising, the oil and gas industry. As with CO2, methane emissions are also rising (see figure 1) and many describe it as the second most important green house gas to mitigate to achieve the Paris Agreement goals. The International Energy Agency describes methane abatement from the oil and gas industry as one of ‘the most cost effective and impactful actions that governments can take to achieve global climate goals’.

We have observed significant activity in the methane innovation ecosystem over the last 12 months. Here is a whistle-stop tour of the blooming innovation ecosystem focused on measuring, monitoring, and mitigating methane including business models, recent deals, and competition.

Attractiveness

Innovators offering methane monitoring services have gained considerable amounts of funding in the last 12 months to rapidly scale operations. Cleantech group spoke to Stephane Germain, President at GHGSat, provider of satellite-based remote sensing technology for the monitoring of greenhouse gas emissions from industrial facilities, who explained “as companies and governments pursue emissions reduction strategies, they are hungry for data. They want to monitor, quantify and verify emissions. For climate intensive industries, such as oil & gas, coal mining and waste management, we provide this useful technology and service to optimize their operations. Governments and financial markets are interested in understanding climate risk and benchmarking companies on their environmental credentials”. This market is largely following suit of the rapidly expanding market for emissions monitoring tools for business and Measurement, Reporting and Verification (MRV) tools with similar drivers and early adopters in hard to abate sectors and financial services.’’

Aside from monitoring, methane leaks can be mitigated, captured and converted into fuel, or flared to convert to CO2. There are numerous ways to tackle methane leaks including:

- Install Plunger: Traditionally, wells are periodically opened to release methane, reliving pressure and making liquids flow. Plunger lifts are installed inside a producing well, as fluid pressure builds it pushes on the plunger which draws up gas and liquid. This enables flow and gas to go directly into the line without the need to vent the methane.

- Vapour Recovery Units (VRUs): small compressors which collect accumulating natural gas

- Blowdown Capture: Blowdowns are when wellheads are opened enabling pressurized gas and liquids to escape. Blowdown capture adds a gas capture element so gases can be reused.

- Install Flares: portable or in-situ combustors, lighting the methane so it converts into CO2, although still a source of CO2 the Global Warming Potential of the gas is reduced.

For example, Frost Methane Labs have developed technologies to survey and measure concentrated methane seeps to quantify their emissions, then deploy Install Flares on these seeps to flare and destroy methane. Frost Methane Labs then sell these services to corporates as offsets. Cleantech Group spoke to Olya Irzak, founder of Frost Methane Labs who explained their combined monitoring and destroy offering “Our remote monitoring system is 6 times cheaper and requires less maintenance and calibration. We tackle emissions from natural sources, coal mines, manure ponds and abandoned landfills and are actively looking to acquire more sites”.

Technologies to prevent, capture or destroy fugitive methane emissions are well established and are usually deployed to prevent economic losses. However, where the economic loss is too small, or solutions are too expensive, further incentives or regulations are still needed. Following COP26 there have been numerous announcements of regulations on methane including mandatory disclosures and tracking. In November 2021, the US announced an ambition to reduce methane economy-wide by 30% by 2030 and proposed regulation which will require oil and gas companies to monitor, detect and repair methane leaks. This same month, the EU announced plans to cut methane from the oil and gas industry which would require companies to report their methane emissions, find and fix leaks and carry out regular surveys.

Recent Deals

- August 2021: Kairos Aerospace, developer of advanced aerial sensors combined with cloud-based analytics to rapidly find methane leaks on a continental scale, raised $26 million from investors DCVC Bio, OGCI Climate Investment and Energy Innovation Capital. The company is planning to use the funding to expand its workforce instrument fleet to support its operations and sales and develop new instruments that will increase sensitivity and improve the utility of data for its customers.

- July 2021: GHGSat, provider of satellite-based remote sensing technology for detection of greenhouse gas emissions from industrial facilities, raised $45 million in series B funding from Investissement Quebec, OGCI Climate Investments and Space Capital. The company plans to use the funds to expand its GHG emission detection array to 10 satellites and 3 aircraft sensors by 2023, as well as to expand its international commercial presence, particularly in Europe and the US.

- April 2021: Carbon Mapper, an NGO focussed on locating, quantifying and tracking methane and CO2 point-source emissions from air and space announced it has launched a satellite program to pinpoint Methane and Carbon Dioxide super emitters.

- April 2021: Crusoe, provider of flare management and reduction services to the natural gas industry, raised $128 million in Series B funding led by Valor Equity Partners. The funding will expand Crusoe’s operations as the Company pursues its mission to eliminate the routine flaring of natural gas and associated methane emissions while delivering low-cost computing infrastructure.

Business Models

Most business models in this space are data-as-a-service, providing data subscriptions or direct facility monitoring. Some also offer project development services for overall methane management.

Innovators are forging new routes to finance action on methane by participating in carbon markets and creating methane capture offsets. Projects include anaerobic digestion for wastes or methane flaring for leaks and oil and gas infrastructure.

In October 2021, Xpansiv, developer of global marketplace for ESG-inclusive commodities and green finance products, partnered with S&P Global Platts to launch a methane performance benchmark targeted at the natural gas market. The issued Methane Performance Certificates will allow oil and gas incumbents to sell gas with zero methane emissions and participate in low-carbon fuel markets. The companies attributed the new market opportunity to upstream drivers from investors for fossil fuel companies to clean up their act.

Competition

There are few Incumbents in this space, those that have been monitoring methane for a long time are governments e.g., Copernicus Sentinel-2 satellite launched by the European Space Agency. There is also strong collaboration in the monitoring space as no one has yet to create a granular picture of global emissions down to an asset level for methane. Therefore, innovators are entering partnerships or open sourcing data to collectively layer data to improve granularity.

Innovators in the methane management space are seeking customers and partners with methane leaks to plug and destroy, however face delays with the slow pace of the oil and gas industry. To address this the industry need to improve industry-wide awareness of methane’s environmental impact and its sources and invest in infrastructure to enable waste-to-value business models so capture technologies can pay for themselves. Additionally, the investment ecosystem can assist by aligning corporate investment with action on climate change, thus incentivising oil and gas companies to invest in technology with the highest abatement opportunities.

To look out for

Drawing more comparisons to the Measurement, Reporting and Verification (MRV) market, we expect innovators to raise large later stage rounds as they look to scale further, while the oil and gas industry need to show stringer drivers to act on methane and regulations proposed need to become effective drivers before companies see clear exit strategies. Greater collaboration between monitoring and emissions management companies also seems highly likely. GHGSat explained clients were next looking to add Carbon Capture Utilization and Storage capacity to their facilities to further their environmental credentials.

The methane innovation ecosystem is rapidly scaling off the back of market and regulatory action on climate change with governments eyeing methane leaks as very low hanging fruit. With national plans to cut methane and rachet action into 2050 we expect continued growth and diversification of solutions in this space.