SPACs in Cleantech: the Python is Digesting an Antelope

SPACs in cleantech is a trend we committed in my Q1 piece – Seven weeks into 2021, there are no signs this 2020 trend is abating – to “revisit regularly in 2021, certainly each quarter”.

And so here we are, with a look back on Q1 and an assessment of the go-forward.

The trend has definitely evolved in some meaningful ways, some of which we will cover in this piece, some we will pick up with more color and depth in an interactive webinar with expert guests on 20 May.

To sum up the state of the market today, I’d use the analogy of a snake swallowing a whole animal, say a python swallowing an antelope. The activity levels have been off the charts- too much, too fast.

Expect a slowing-down for now, while the market works through the combination of a vast pipeline of deals, backed-up in the PIPE market, and the knock-on effects of greater oversight from the SEC.

Let’s start at the SPAC end of the pipeline. Q1 2021 alone blew away the records set in 2020.

The 248 SPAC IPOs in 2020 exceeded the 225 for the whole of the prior decade.

At the time of writing, 2021 has seen more than 300 SPAC IPOs, raising gross proceeds in excess of $100bn (compared to the $83 billion raised in the whole of 2020), according to SPACInsider.com. And there are a further 265 SPACs who filed for IPO during Q1.

There is, quite simply, a wall of SPAC capital seeking targets.

In February, I cited 330 SPACs to be out there looking, of which, based on announcements to that point, I reasoned about 30% might end up doing a deal with a “cleantech-relevant” target.

70% of the 2019-2021 listed SPACs are still in the search phase. There are 428 of them in total today, carrying an average of $330m in cash proceeds. That sounds like $140bn of capital, of which say $30-40bn might be expected to find a sustainable home in the cleantech innovation theme.

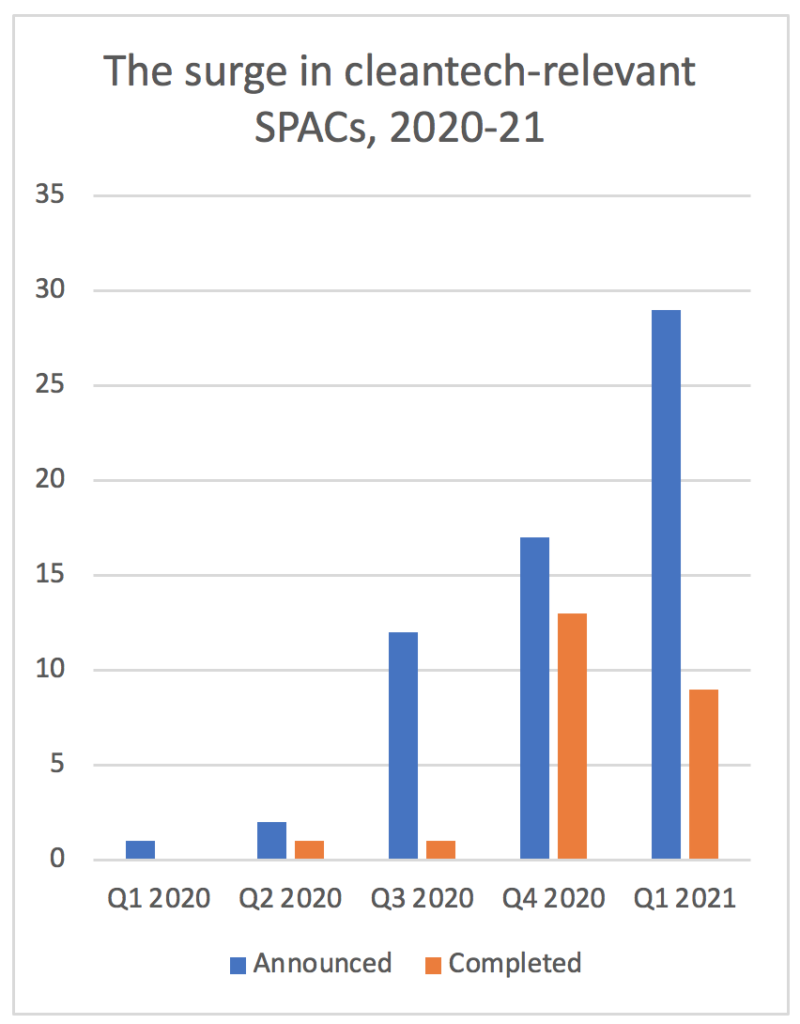

Q1 2021 has seen the surge of cleantech-relevant SPACs continue.

Two key things to note from the chart:

- We counted 29 more announcements of SPACs achieving definitive agreements with cleantech-relevant targets in Q1 2021, taking the total number to 61 since Nikola in Q1 2020 (note: we revised upwards from 30 to 32 for 2020 activity). That has the cleantech theme maintaining its 33% share of all the announced SPAC activity in 2020-21.

- Only nine SPACs fully completed in Q1 2021 (compared to 13 in Q4). That speaks to the backed-up state of the market today.

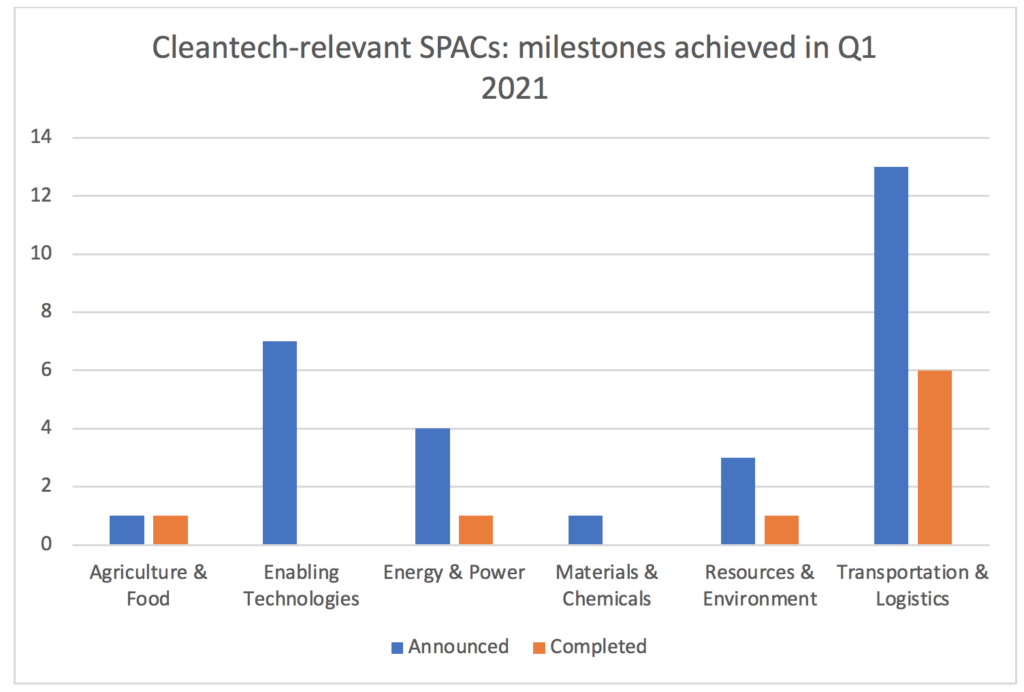

One of our expectations expressed in the last piece was that we would start to see diversification of SPACs in cleantech, away from EVs and the electrification of road transport mega-trend

For the most part, frankly, we are still waiting!

Transportation & Logistics has continued to predominate in the new SPAC announcements in Q1, accounting for 13 of the 29 new agreements reached, with more charging plays (e.g. EvGo and Volta), and more EVs in various market categories, from cars to SUVs, buses to trucks (e.g. Faraday Future, Lucid Motors, Proterra, REE Automotive, Xos).

That said, SPACs also went airborne, inasmuch as Q1 saw urban air mobility companies, Archer Aviation, Joby Aviation, and Lilium all announce definitive agreements to reverse-merge with a SPAC, adding significant tailwind force to the idea that the future of shorter-haul air travel may be in for significant change from, say, 2025 onwards.

We are seeing other plays on the electrification trend via batteries (Enovix and FREYR) and in terms of the vast resources the vast electric build-out will require. Of note would be the SPAC deals with two Canadian companies, DeepGreen (and its access to the world’s largest estimated resource of Battery Metals for EVs on the floor of the Pacific Ocean) and Li-Cycle (the Lithium-ion battery recycling company)

Even the Enabling technologies category is often connected to the future of mobility and the connected and autonomous vehicle of the future.

I have the clear sense, in looking at the numbers and from talking to a number of people close to the transaction action, that the SPACs market has moved into a new phase.

The market feels like it is taking a breather right now for two fundamental and practical reasons.

First, very simply, the sheer volume of transactions in the queue has overwhelmed the market and time to absorb and adjust is needed – hence, the python swallowing a deer analogy.

- There are only so many deals key investors in the PIPE market like say BlackRock, Fidelity and T. Rowe Price can process and diligence in any one month. And we are fast reaching the point where they themselves need liquidity and capital to be recycled from the deals already done.

- Plus, the advisor community (bankers, auditors, lawyers, etc.) is also over-capacity on SPAC deals, real and prospective.

Second, the size of the SPAC “gold rush” is now inevitably (and rightly) attracting closer scrutiny from the Securities and Exchange Commission (SEC).

- The April 12th announcement from the SEC that SPAC warrants should not always be treated as equity investments, but as liabilities, has caused some pause for thought. This will impact some transactions that have already occurred and that were in process. It is not a showstopper by any means – it’s an accounting principle – but it is something that needs to be adjusted into future thinking and valuations and terms between the sponsors, existing shareholders and PIPE investors.

- Plus, just as I was finishing this piece we learned, via reporting from Reuters, that the SEC is considering issuing new guidance on when safe harbor applies to forward-looking statements by companies going public via SPAC.

These current conditions have put a major brake on April activity.

That said, the wall of potential SPAC capital for cleantech remains and will look to move forward, once the python has digested and rested, and the new rules of the game have been set and adjusted to, ahead of the next phase.

What next, what to pay attention to?

I think a very reasonable bet would be to expect a more sober and discerning market in the coming weeks and months, compared to the early exuberance of 2020.

Given the backed-up state of the market right now and the higher scrutiny from such as the SEC, it would seem reasonable to expect the following to be the key issues and questions of the coming weeks and months. Expect our May 20 webinar to revisit and add color to many of these.

- Has the window of opportunity closed on companies at the pre-revenue, with few proof points and a handful of cancellable contracts, end of the spectrum?

- Should we expect sponsors, fearful of potential future lawsuits, and the professional service firms, keen to work on transactions that have the highest probabilities of happening, to drive more SPACs towards safer, more predictable plays? (the standout example of this nature from Q1 was arguably Ardagh Metal Packaging, a spinout from the listed company, Ardagh Group, headquartered in Ireland).

- How long does the python take to absorb the antelope? What mood and mode will it be in, after some rest?

- How do the shares of the companies listed via SPACs perform post combination and shares being registered to trade? Do PIPE investors get good liquidity? What do founders and venture-stage shareholders do as the first of the 2020 transaction reach the end of their lock-up periods?

- Is there a change in terms and conditions? Who flexes their muscles more and most?

- Do we see longer lock-ups and terms to align to the long-term value creation inherent in many of the announced transactions? (In Q1, for example, it was noticeable Joby’s terms included terms like f-year lock-ups for founder and other major shareholders and earnouts pegged to a market capitalization increase that equates to about five times today’s implicit value).

- What roles do incumbent Corporations play in these SPACs? (we sensed more involvement in Q1 PIPEs and the like from strategics).

- Will we see greater evidence of the geographical and sectoral diversification we anticipate? Ag and Food was an area we highlighted last time but Q1 “only” saw the completion of AppHarvest and the announcement of Aerofarms (whose CEO is joining us on May 20’s webinar), a multiple-times Global Cleantech 100 company.

Of the 61 announced to date, nearly 25% have been alumni of our long-running Global Cleantech 100 program. Who will be next?