The Electrolyzer Race: The Tortoise Versus the Hare

There has been a substantial increase in both the quantity and volume of investment deals in the electrolyzer market since 2021. Nevertheless, the cost competitiveness of large-scale green hydrogen production – hydrogen produced from renewable energy with electrolyzers—remains a challenge when compared to gray hydrogen, which is produced from fossil fuels without carbon capture.

The Inflation Reduction Act (IRA) has been the greatest step forward policy-wise in addressing this issue by creating a tax credit for up to $3/kg of green hydrogen with an inflation adjustment of 2% per year, for the first 10 years of operation (their lifetimes are typically up to 30 years). However, the tax cuts run only through 2032, so projects starting up in 2023 would benefit from the full 10-years’ worth of credits, while plants opening later would receive progressively less.

The race to reach the magic $1/kg production cost for green hydrogen is on and will likely be won by incumbents in the next few years. Some estimates show that the price levels for some U.S. regions have already declined as low as $2.5/kg. The incumbents, such as ITM Power, Plug Power and Thyssenkrupp, have locked in their choice of technology and are developing gigafactories to scale up production.

Scaling up capital intensive production will likely limit the incumbents’ ability to innovate, leaving space for new electrolyzer designs to enter the market. Recent experience shows that the scaling process has not been without growing pains, including delays in product delivery and failure to offer performance guarantees. As a result, the shares of many pure-play green hydrogen companies have slid this year.

However, the race is not always won by the hare as there is scope in the market for disruption. In the second half of the decade, new electrolyzer designs that can demonstrate marked efficiency improvements and price reductions will gain foothold in the market, following the, by then, well-trodden path of scaling up set by current incumbents.

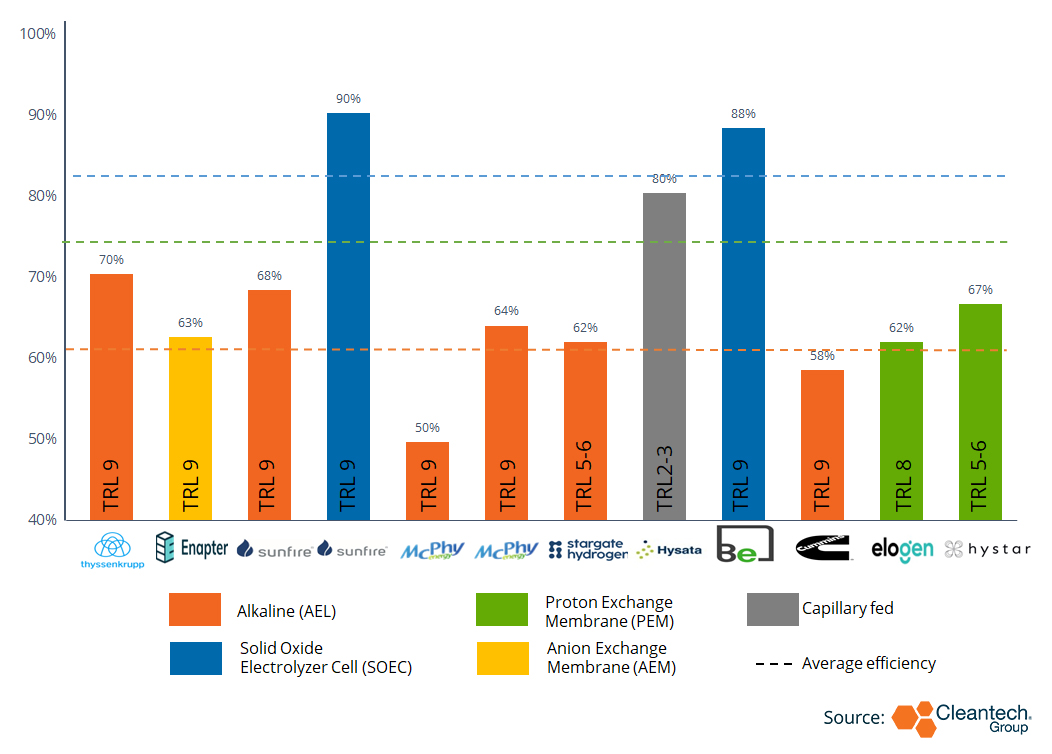

Innovation focuses on overcoming some of the limitations of the electrolyzer technologies that currently dominate the market – alkaline and PME – such as reducing corrosiveness, increasing efficiency, or dependence on platinum group metals such as iridium. Most alkaline water electrolysis (AWE) and proton exchange member (PEM) technologies currently have a low heating value (LHV) efficiency of up to 75%, while some of the newer electrolyzers have LHV efficiency of well over 80% (e.g., Bloom Energy, Hysata).

Electrolyzer System Efficiency (LHV)

Innovators like AquaHydrex, are developing improved alkaline models that are optimizing the balance of plant (BoP) and eliminating a flowing electrolyte loop that causes corrosion. BoP accounts for roughly 20% of all system costs for alkaline electrolyzer. UK-based Oort Energy is developing technology that reduces hydrogen crossover into the oxygen loop, increasing safety, while improving the performance of the membrane. Electric Hydrogen, from the U.S., is trying to gain an edge with a vertically-integrated business model, driving costs down across the value chain. Research from the International Renewable Energy Agency (IRENA) shows that going from 10MW/year scale to 1GW/year allows for a 70% potential cost reduction, while semi-automating stack assembly can yield a 90% cost savings.

Cost savings can also come from increased standardization on the system level, which would enable developers to buy off-the-shelf components rather than produce them themselves. Classification company DNV last February launched a joint industry project with 18 industry partners to promote standardization in electrolyzers. Previously, standardization has played a key role in decreasing wind and solar PV project costs.

Many innovators have eschewed those models altogether and are working to decarbonize hard-to-abate sectors with solid oxide, which has higher efficiency than any commercial electrolyzer. However, solid oxide electrolyzers operate in a 500°-900° temperature range, while most other electrolyzers work at ambient temperatures. The specialized application of solid oxide technology is primarily observed in heavy industries, such as steel manufacturing, ammonia or chemicals production, and refining.

In these industries, a crucial aspect to consider is the utilization of waste heat. The incorporation of thermal energy into the functioning of a solid oxide electrolyzer in order to enhance the power supply results in improved electrical efficiency of the equipment and significant reductions in operating expenses.

Finally, electrolyzer manufacturers like Enapter or Versogen that are developing anion exchange membranes (AEM) are attempting to circumvent the necessity for noble metals used in PEM at the same efficiency rate. This process demonstrates efficacy even when implemented on a smaller scale, rendering it appropriate for decentralized applications. Despite gaining significant interest from venture capitalists, it is unlikely that the technology readiness level (TRL) of this particular type will reach the levels of PEM or alkaline until the latter part of the 2020s.

While the question of who reaches price parity for gray hydrogen first remains to be seen, global market dynamics are showing a consensus that electrification is not enough, and we need affordable green hydrogen to reduce carbon emissions in the hard-to-abate sectors. While the jury is still out on exactly which end-user markets will successfully adopt green hydrogen, it is clear that it can displace the 94 tonnes of gray hydrogen that is being used across industries globally. Electrolyzers are a key component to making this possible.