The Voluntary Carbon Offset Market – Can We Support Rapid Growth?

The demand for quality carbon offsets is at an all-time high due to unprecedented enthusiasm to act on climate change from the business community. This is due to three key drivers:

- Corporate commitments and the race to net-zero emissions

- Investor and customer pressure to disclose and act on emissions

- Mandatory emissions disclosures (see our insight on emissions disclosure data tools).

As a result, the voluntary carbon offset market is rapidly expanding. In 2019, the Ecosystem Marketplace found 74% of project developers found a buyer for some, if not all, their carbon credits prior to issuance.

Many barriers still exist for buyers Including:

- The high cost of nature-based solutions

- Methods to measure and monitor capture and storage

- Ensuring a long-term and stable supply of offsets

- The lack of a carbon credit reference price to base transactions on.

As such, Intermediaries and innovators are seeking to formalize and structure the market to reduce barriers to entry. There is a flurry of innovation and business activity around this aim, underlining how innovators are building the market infrastructure and ultimately creating a thriving Voluntary Carbon Offset Market (VCM).

Attractiveness

In September 2020, Mark Carney, the UN Special Envoy for Climate Action and Finance Advisor to UK Prime Minister Boris Johnson for COP26, launched the private-sector led Taskforce on Scaling Voluntary Carbon Markets (TSVCM), sponsored by the Institute of International Finance (IIF). The TSVCM estimates demand for carbon credits could increase 15-fold by 2030 to $50 billion. Chair of the TSVCM, Bill Winters, Chief Executive of Standard Chartered outlined the aims of the group,” By scaling voluntary carbon markets and allowing a global price for carbon to emerge, companies will have the right tools and incentives to reduce emissions at least cost.”

Improvements in hard to abate industries, like steel and cement, will be essential in the transition to the low carbon economy. As they contribute significant emissions, offsets provide external opportunities to decarbonize business operations. In March 2021, steel major Arcelor Mittal began offering its customers the opportunity to offset the emissions created when customers process raw materials (Arcelor Mittal’s Scope 3 emissions).

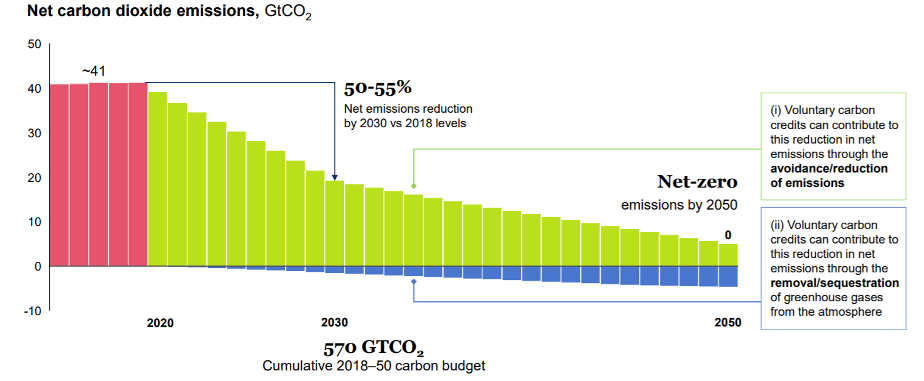

Carbon offsets can also finance carbon removal projects or ecosystem protection with few commercial or monetized outputs e.g., protection of mangrove forests. Carbon removal also plays a key role most scenarios to achieve the goals of the Paris Agreement (see figure 1).

However, it is important to note the risks of net emissions’ reductions via carbon offsets and wider criticism of carbon markets, including:

- The risk of double counting.

- Ensuring permanence of sequestered Carbon.

- Offset purchases may lead to avoidance of mitigation activities.

- Certification bodies like Gold Standard are slow to recognize new project types like Carbon. Capture.Usage and Storage (CCUS). As a result, initial sales of these offsets are uncertified.

- transparency and inclusion in overarching figures.

- Site-specific offsets may conflict with other land use activities like space for food production.

Innovation can help mitigate the risks of offsets, while also creating offset projects (eg CCUS) and ensuring the market can scale without compromising quality.

Business Models

Data tools are often the key to unlocking a thriving and transparent carbon offset market. Below are some of the key emerging technologies across the value chain:

Remote carbon sequestration estimates and monitoring

Innovators are using satellite data or LIDAR to estimate the carbon capture potential of prospective sites and autonomously monitoring carbon storage to ensure permanence. This automation is reducing the labour costs of offsets and so streamlining the process of monitoring variable nature-based offset projects over time.

- March 2021: Pachama, developer of satellite and LiDAR-based carbon storage estimation solutions, raised $8 million in Project Financing from Argentine e-commerce corporate Mercado Libre’s $400 million sustainability bond. Pachama earlier raised $5 million in Series B funding from strategic investors Amazon, Breakthrough Energy Ventures, Aglaé Ventures and Angel Investor, Serena Williams.

- January 2021: SilviaTerra captures 200,000 tons (15%) of the Microsoft carbon removal RFP. In January, they raised a $4.4M seed round co-led by Union Square Ventures and Version One Ventures. SilviaTerra’s Natural Capital Exchange is a forest carbon marketplace driven by satellite-based measurements of every acre of forest every year.

We spoke to Max Nova, the CEO of Silvia Terra, who explained,”Hundreds of millions of acres of forests are excluded from traditional forest carbon projects. SilviaTerra’s measurement technology lowers the barrier to entry so that landowners of all sizes can be part of the climate solution. By democratizing access to forest carbon markets, we’re unlocking a gigaton-scale supply of new carbon credits.”

Pricing

In January 2021, the TSVCM released its roadmap for scaling the VCM and its key recommendation to establish ‘core principals’ of what a carbon credit is to then ‘establish a carbon credit price on which transactions can be constructed’.

Ecosystem Marketplace, an initiative of NGO Forest Trends, has been polling its global network of project producers, intermediaries, and investors in the VCM, for over fifteen years to provide annual reference prices and assessments of the health of the VCM. In efforts to realize a more near-real time carbon credit reference price, they are in process of launching an online data platform for its members to regularly contribute to following any carbon credit sale and delivery. This data will feed into its live dashboard enabling dynamic pricing and market transparency.

Cleantech Group spoke to Stephen Donofrio, the Director of Ecosystem Marketplace at Forest Trends, who explained, “We have passed an inflection point as corporates are increasingly lining up their sights to invest in the long term with ambitious goals such as net zero. At the same time, we are seeing supply-side growth to meet the demand as our membership base and those we are surveying has increased more than threefold. Our focus now is on expansion, to make the data real-time to support developers, intermediaries, start-ups, corporates and governments with market transparency, voluntary action and complementary regulation.”

Competition

As demand is predicted to outstrip project supply in a year or two, the competitive ecosystem is collaborative at this stage but increasingly crowded.

Cleantech group have spoken to numerous clients interested in this space, particularly those with business models which are hard to abate like oil & gas, and airlines. Many of these players are keen to secure a reliable supply of high-quality, certified offsets. For example, in September 2020 Direct Air Capture developer, Climeworks, entered a vendor partnership with Audi to remove 1,000 tons of CO2 from the Atmosphere on behalf of Audi.

Look ahead – Unlocking Blue Carbon

Corporate customers have invested in earlier stage offset projects, funding R&D, recognizing the need to invest in innovation to achieve ambitious emissions reduction goals. One such area is Blue Carbon, the carbon sequestered in coastal and marine ecosystems.

- September 2020, Shopify invested in Planetary Hydrogen, producer of hydrogen from the ocean while capturing and storing carbon dioxide which is turned into bicarbonate that fights ocean acidification, with the intention to purchase negative emissions generated by Planetary Hydrogen’s pilot plant which will begin operation in 2022.

- June 2020: Carbix, developer of advanced enhanced weathering technologies which transforms CO2 into raw materials, was selected to join the Indie Bio life sciences accelerator program.

However, there is huge variability of carbon sequestration potential between habitats and overtime, making it difficult to estimate or compare carbon potential of projects. Additionally, coastal ecosystems are poorly understood, comparisons of lab to field-based studies show significant variability in capture potential. Thus, further R&D is needed to unlock commercial blue carbon offsets.

The unprecedented demand for carbon offsets has lit the match which may propel the VCM into a thriving and tradable carbon market. Although the drivers are encouraging, carbon markets have failed before and the multiple barriers and risks still exist. Innovation, regulators and intermediaries will all need to sustain this momentum to build the essential infrastructure for a sustainable and thriving VCM.