We’ve Changed How We Think About Resources and the Environment

As the cleantech landscape continues to evolve, so does our understanding of it. To better capture this evolution, we’ve decided to divide the Resources & Environment industry group, established in 2018, into two distinct categories within our taxonomy:

- Resources & Environmental Management

- Waste & Recycling

This division allows for more precise analysis and insight into cleantech. Here are five key observations from our new analysis that shed light on the industry’s evolution over the past five years that offer insights into its future trajectory:

1. Corporate action on climate change has created new markets in environmental monitoring, including voluntary carbon offset market tools, climate risk analytics, environmental monitoring solutions and services for businesses, such as emissions monitoring and lifecycle analysis of products.

These all branch from investor, public, and regulatory drivers for large corporations to get on top of climate change. From corporate commitments to reduce emissions to increasing climate risks, companies need to mitigate. If corporations have any future, they need to plan for climate change and innovators such as Persefoni and Jupiter Intelligence, who didn’t exist in 2018, are helping to streamline this process.

We expect consolidation in this market, which is highly saturated, but we also expect continued innovation as innovators diversify to cater their products to specific industries, applications, and different environmental metrics, e.g., biodiversity.

2. The disruptor of 5 years ago is now the incumbent. In 2018, many technologies were replacing manual or paper-based systems, whereas today more and more technologies are now replacing or complimenting technologies.

For example, the incumbent approach to wildfire prevention today is satellite monitoring and cameras. While these enable remote monitoring for early detection, there are high costs and blind spots. Newer AI applications can guide any sensor where to look, reducing costs and blind spots. The pace of technological change is speeding up.

3. Climate risk & resilience continue to see underinvestment. As physical climate risks intensify, we expect a greater focus on prevention and resilience innovations, e.g., Kettle. Although at present, funding and partnerships are few and far between, while customers are mostly cash-strapped public entities and stubborn insurance companies. As such, losses (human, environmental, and economic) will likely get worse before they can get mitigated.

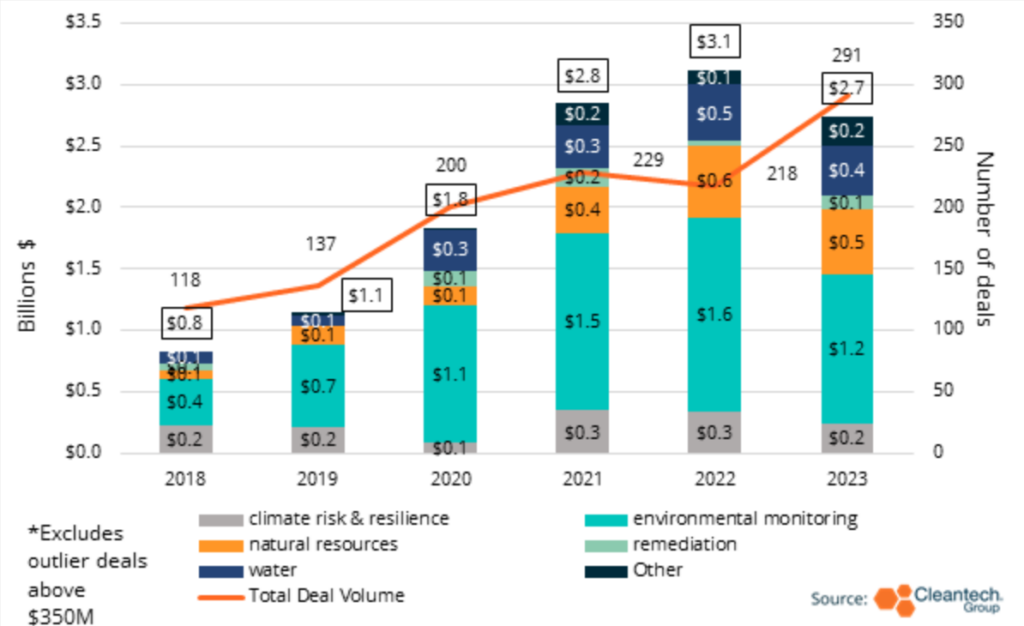

Resources & Environmental Management

The new Resources & Environmental Management industry group (Figure 1) includes innovators who are:

- Improving the sustainable use of natural resources including mining, oceans, water, and forests

- Solutions to monitor environmental impact such as emissions and air pollution with environmental monitoring and climate risk

- Finally, the sector includes remediation activities, including nature-based carbon removal and climate resilience

Figure 1: Resources & Environmental Management

4. Recycling companies are actually on the up. Although the numbers show a decline in investment amount($800M), the overall trend is that of maturity with rounds being omitted due to the $350 outlier exclusion in our graphs. This is especially true with U.S.-based battery, metals, and chemical plastics recycling innovators. In 2023, provider of battery recycling and critical metals recovery, Redwood Materials raised $1B in a Growth Equity round; while steel scrap recycler, Hybar, raised $370M in a Growth Equity round.

Other omitted rounds include PIPE and follow-on offerings as well as project financing and structured debt. For example, developer of tracking system for retailers to divert food waste to anaerobic digesters, Divert raised $1B in project finance from oil and gas company, Enbridge, to support an infrastructure expansion across North America to convert food waste into RNG.

These companies are in later stages of development building infrastructure and scaling – however, mostly in the U.S. and Europe where critical material supply security are of national interest and regulations and corporate action on plastics is driving recycling infrastructure investment.

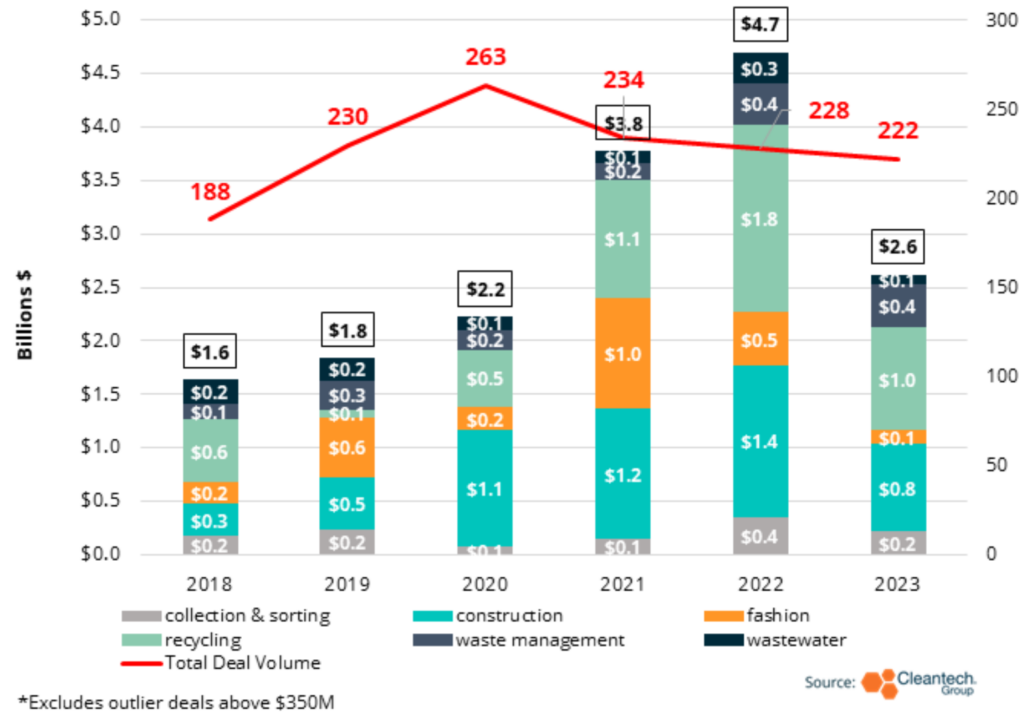

Waste & Recycling

The new Waste & Recycling industry group includes innovators who are improving waste management including:

- Collection & sorting technologies optimizing how much gets collected, cleaned, and processed

- Recycling innovations to improve waste recovery rates and optimize waste-to-value

- Wastewater technologies, which are improving how potable water gets cleaned for discharge into the environment or for reuse

- Innovators in fashion are reducing pollution in the industry, from reuse and resale business models to production using deadstock

- In construction, innovators are streamlining operations to reduce rework costs and enable reuse and resale

Figure 2: Waste & Recycling

5. Fashion majors are failing to scale innovation, while disrupters continue to mature. We hold justified alarm for fashion innovation, observing a drop in investment into textile recycling innovators, whilst scaling and commercialization opportunities remain limited. Notably, Renewcell filed for bankruptcy this month following ‘lower than anticipated sales volumes to fibre producers’ in November. Renewcell’s chairman, Michael Berg, cited ‘the lack of leadership’ and slow ‘pace of change in the fashion industry’ as contributing factors.

2021 saw a peak of investment activity in fashion, bolstered by the scale-up of B2C resale platforms including Vestiaire Collective which raised two Growth Equity rounds of $216M and $250M for APAC expansion, following a 150% increase in orders from the region. Vinted also raised a considerable amount in 2021, $303M in Growth Equity, leading to a post-money valuation of $4.5B. Since, we have monitored multiple new resale apps and platforms but no longer include them in our figures as they no longer quality as ‘innovative,’ however sustainable.

We have observed an uptick in earlier investment into B2B platforms seeking to streamline the shift from cradle-to-grave to cradle-to-cradle and facilitate circular business models. For example, Trove has created a recommerce operating system and is working with brands such as allbirds, Carhart and ON to facilitate return and resale of their products.

The cleantech landscape’s journey of evolution is exemplified through the division of the Resources & Environment industry group into Resources & Environmental Management and Waste & Recycling categories. This move reflects the sector’s increasing complexity and diversity. This modernization of our taxonomy is aimed at enhancing the clarity and accuracy of our data sorting and signposting, ultimately enabling more meaningful analysis for our clients and stakeholders.