Are Mining Majors Ready to Take Full Advantage of Exploration Technologies?

Mining majors have underinvested in innovation, having gutted R&D programs since the 80’s. Although investment is increasing, compared to similar industries such as oil and gas, innovation investment remains significantly lower. Today, external factors including inflation and declining ore grade are increasing operational costs and high demand for critical materials with better ESG credentials. Mining majors must look for ways to save costs, explore new extraction technologies, and look for better ways to scale such technologies.

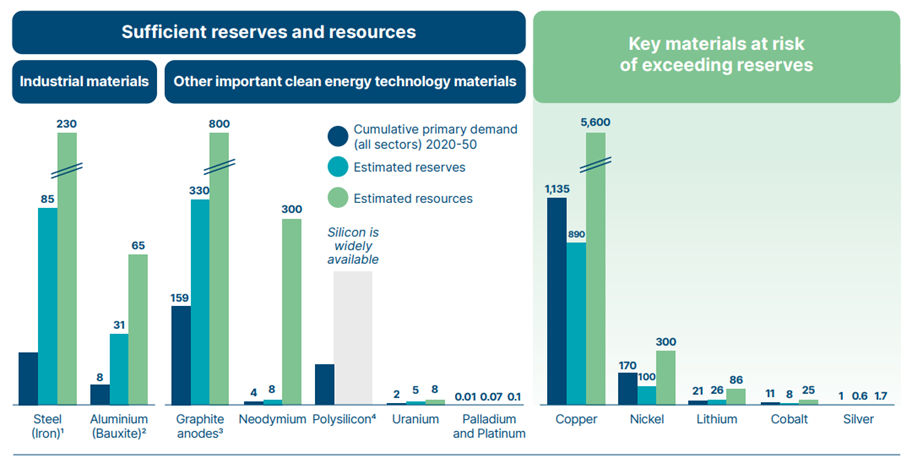

Less than 1% of mining exploration projects progress to a commercial mine. Exploration is also increasingly expensive and yields poorer results due to decreasing ore quality. Meanwhile, the energy transition will require 6.5B tonnes of additional materials; 95% of this is steel, copper and aluminium, where known reserves are sufficient to meet demand. The other 5% are critical materials where there a gulf between predicted demand and known reserves (Fig. 1), thus requiring exploration for critical materials.

Figure 1: Cumulative Primary Demand 2022-50 From the Energy Transition and Other Sectors Compared to Estimated Reserves and Resources

Source: ETC, Material and Resource Requirements for the Energy Transition, 2023

Technologies

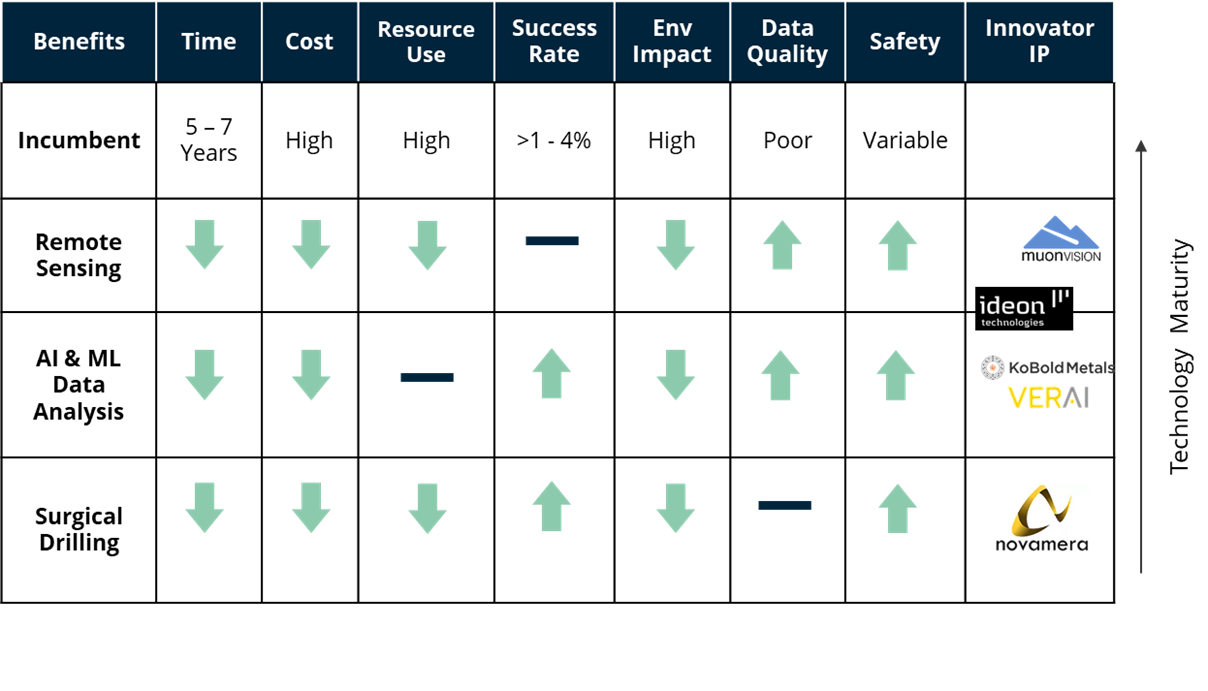

Exploration technologies are being stacked by miners to provide all benefits across mining exploration as no one technology can deliver all benefits, aside from improved safety (Fig. 2). Innovators are also stacking technologies, usually established remote sensing capabilities, offering end-to-end exploration or drilling services. Technologies poised to transform exploration include:

- Advanced sensing (Muon, LiDAR and Hyperspectral) technologies are providing more detailed and accurate estimation of ore quality, characteristic, and location, e.g., they can visualize underground ore quality to target drilling.

- AI and ML analysis software are being stacked with advanced sensors, analyzing large data sets to predict ore location and improve chances of discovery, e.g., they can predict and model ore location based on similar mines/topographies more accurately.

- Precision extraction tools are modular, reducing OpEx, accessing smaller, challenging deposits, e.g., a long, small vein of gold in a protected forest.

Figure 2: Benefits of Low-impact Exploration Technologies for Miners

Recently, mining majors have made significant moves in leaning towards innovation:

- 2020: BHP launched BHP Ventures and has 18 portfolio companies across mining exploration and new energy.

- 2019: Vale created an artificial intelligence center, seeking to scale and integrate AI across its operations.

Challenges of Mining Majors

Challenges still exist in rolling out new technologies in mining due to the large scale of projects and the inflexibility of mines to facilitate a pilot. Any small delay in a large mining operation can cost millions. It is also unclear whether internal investments and structures have been established to scale after pilot stages and to bolster knowledge and network gaps from historic underinvestment.

Unlike the oil and gas sectors who often collaborate to scale innovation with initiatives like the oil and gas climate initiative (OGCI), mining majors have viewed the strong competition between them as reason to work in silo on innovation. Due to this strong competition, there are also concerns around IP protectionism and acquisitions of innovators to hold strategic advantage rather than enable scaling.

Whoever Has the Rock Wins in Exploration

We, therefore, see innovators become smart mine owners rather than the traditional SaaS business model, which can limit scale. These AI and ML data analytics innovators focus exclusively on exploration in a mine’s lifecycle, which risks diluting the value of their discovery, so they are first acquiring mining licences and then partnering with majors:

- Some innovators are offering end-to-end exploration services (Kobold Metals) to hold greater ownership/value of the mine discovery, but this asset heavy, high OpEx approach leaves greater exposure to external impacts, such as rising labor costs or red tape from resource nationalism).

- Others have an asset-light approach, offering equity shares in exchange for exploration services and finance (VerAI). This approach dilutes the value of the discovery, but the innovator is protected from external factors, while they also benefit from expertise, contacts, and operational efficiency from partners.

These independent approaches may divert some of the challenges when working with mining majors and may finally see innovators achieving impactful scale in exploration.

Looking Ahead

Innovators will need to be selective in co-development with majors (which can narrow focus and limit scaling potential) and be cautious about mergers seeking to hold IP for strategic advantage. Mid-tier miners will be good first customers for innovators, being more cash strapped and looking for efficiencies, whilst also being agile and looking for a competitive edge.

Mining majors who wish to capitalize on the full benefits of innovation must ensure internal structures are established to scale innovation beyond pilot, mitigate IP protectionism, and explore tech uses beyond their own operations and the mining industry.

It’s clear the mining industry is maturing when it comes to innovation but with oncoming challenges of supply pinches expected with rising demand for critical materials, flexibility in an inflexible system is required. With greater demand for critical materials, there is an increasing global trend of resource nationalism (e.g., Chile nationalized its lithium industry).

For innovators already strongly aligned with mining majors, it will be costly to pivot marketing to state-owned companies. Although with greater control of mines by governments who want to improve mining’s ESG performance, the use of exploration technologies, which boost the case for licenses to operate, may prove an advantage.