Cleantech Trends in APAC: A Look Back at 2023 and Forward to 2024

Our annual APAC Cleantech 25 was released on April 18th, 2024 – this is always a great opportunity to zoom in on the region and reflect on its importance in the global cleantech ecosystem. This year’s list demonstrates a deepening of trends observed a year ago – where the region was shifting heavily toward an emphasis on new energy and associated materials, electric mobility, and technologies for circularity. Reflecting on 2023, APAC distinguished itself by actually expanding venture and growth investments in cleantech. This contrasts to other regions, where a minimal drop was deemed a success.

The apparent drop-off outside of the Asia-Pacific is partially attributable to certain policy changes, especially the U.S. inflation Reduction Act (IRA) and the European Union Net Zero Industry Act that have made it easier for innovators to access financing without relying only on equity, for financing new and innovative cleantech, especially in the U.S. where the IRA has allowed many innovators to start to transition into raising debt for their growth. There is an additional point to make, however, that there are certain areas of cleantech innovation in APAC that have benefitted from a more mature demand pull (see the examples of solar and batteries in China below) and were still able to continue development while their overseas peers accelerated.

Interestingly, the first quarter of 2024 has shown a slowdown in APAC, though it’s premature to determine if this will be a persistent trend or merely a temporary dip. We will be looking closely to see if this will be a protracted trend or just a blip on the radar.

Digging Deeper into the Deep Tech Stack

Throughout 2023, APAC saw a marked shift towards deeper technology sectors crucial for a new energy economy, namely innovation in solar, batteries, hydrogen production, and the materials required to increase efficiency.

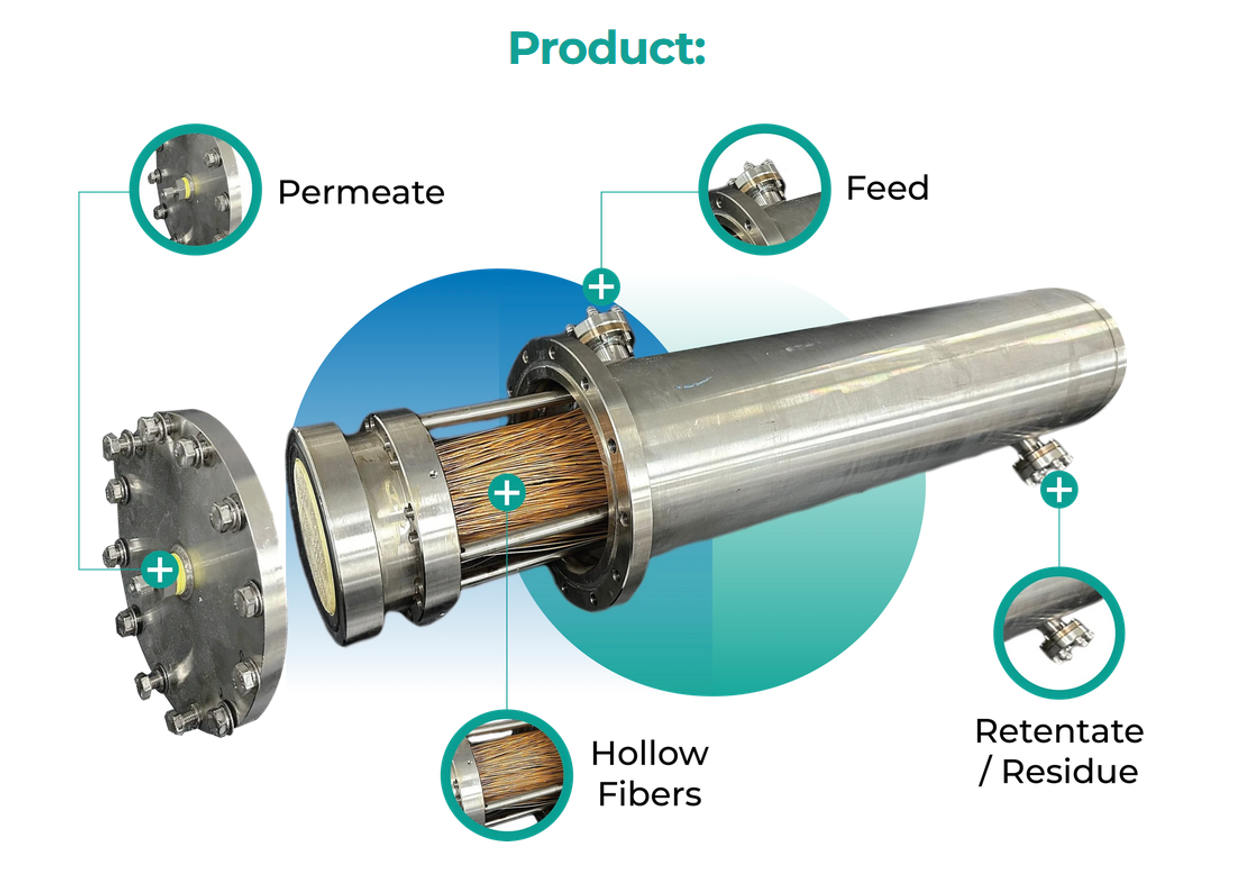

Notable developments reflected in this year’s list of 25 include advancements in hydrogen production and separations technologies. Singapore was especially active here – see Sungreen H2’s electrolyzer electrodes that have designed out platinum group metals, DiviGas’s polymeric membranes to separate hydrogen from mixed gases, and SepPure’s chemical-resistant nanofiltration equipment.

Divigas’s Hydrogen Separation Membranes

Watch this space closely — innovation to tackle the manufacturing cost of hydrogen production equipment is popping up all over the region. Case in point: India’s Newtrace landed on the list this year with a product that seeks to maximize use of abundant materials in electrolyzers, potentially dropping costs by up to 30%.

Newtrace’s Electrolyzers with Abundant Electrocatalysts

Solar and Energy Storage – China Retains its Position

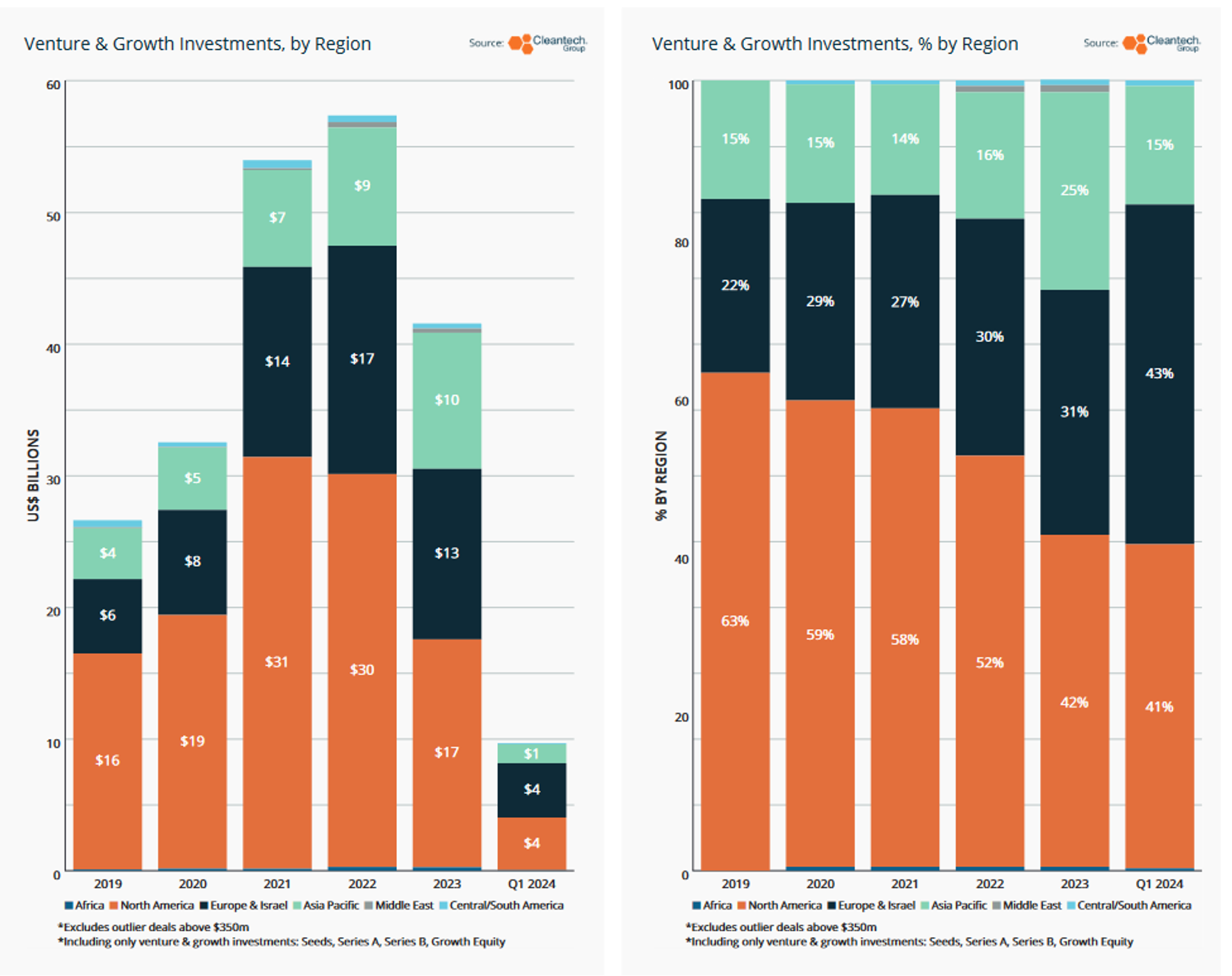

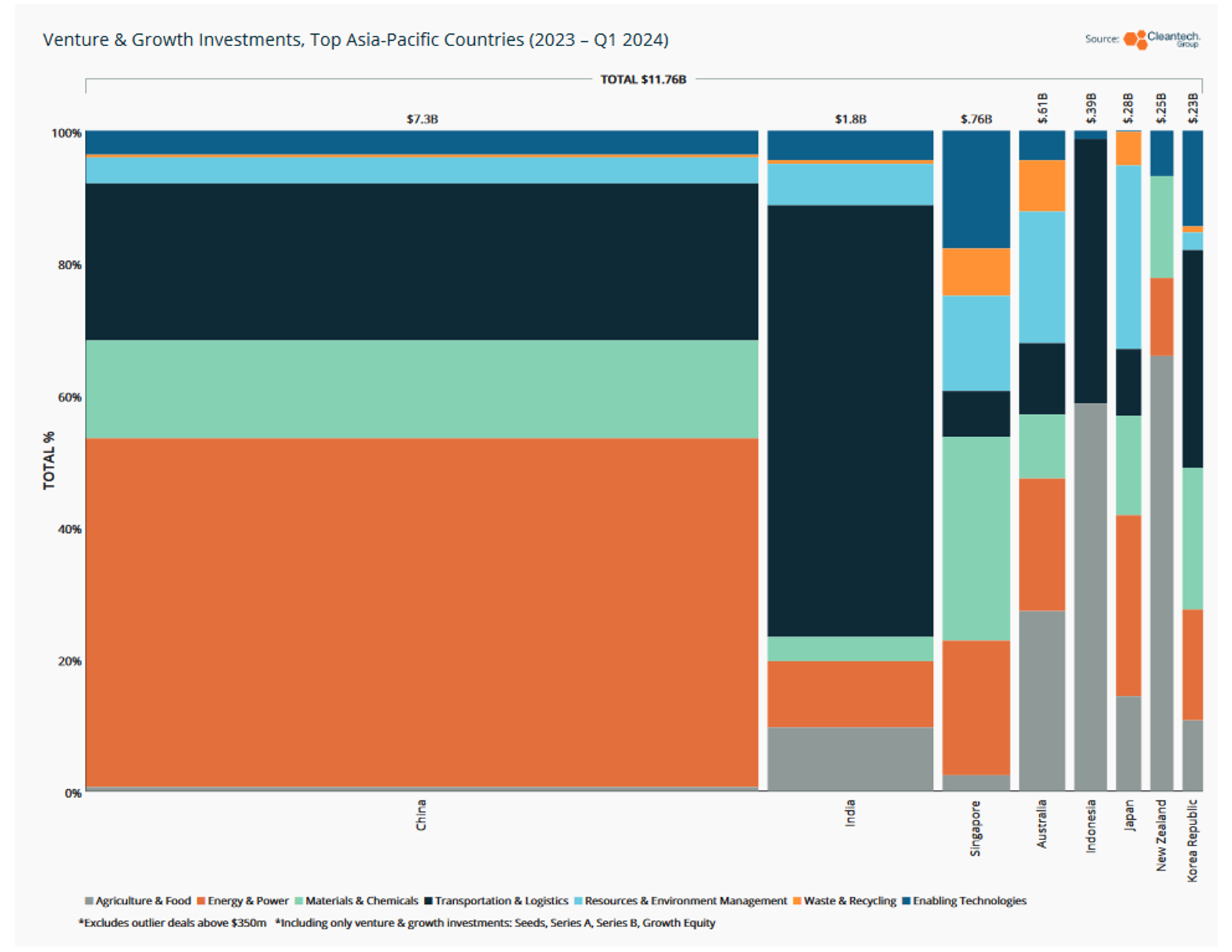

China continued to dominate the investment landscape, capturing 63% of the region’s venture and growth funding in 2023, slightly up from 59% the previous year. Once again, engagement with Chinese cleantech innovation was most observable in the Energy & Power space. This is not surprising, given that China’s national government has put a public emphasis on developing the “New 3” industries of solar power, electric vehicles, and batteries.

In 2023, the “New 3” accounted for all of China’s 2023 national investment growth and nearly half of GDP growth. And you can see this reverberating throughout the economy in generating more demand pull for innovative technologies.

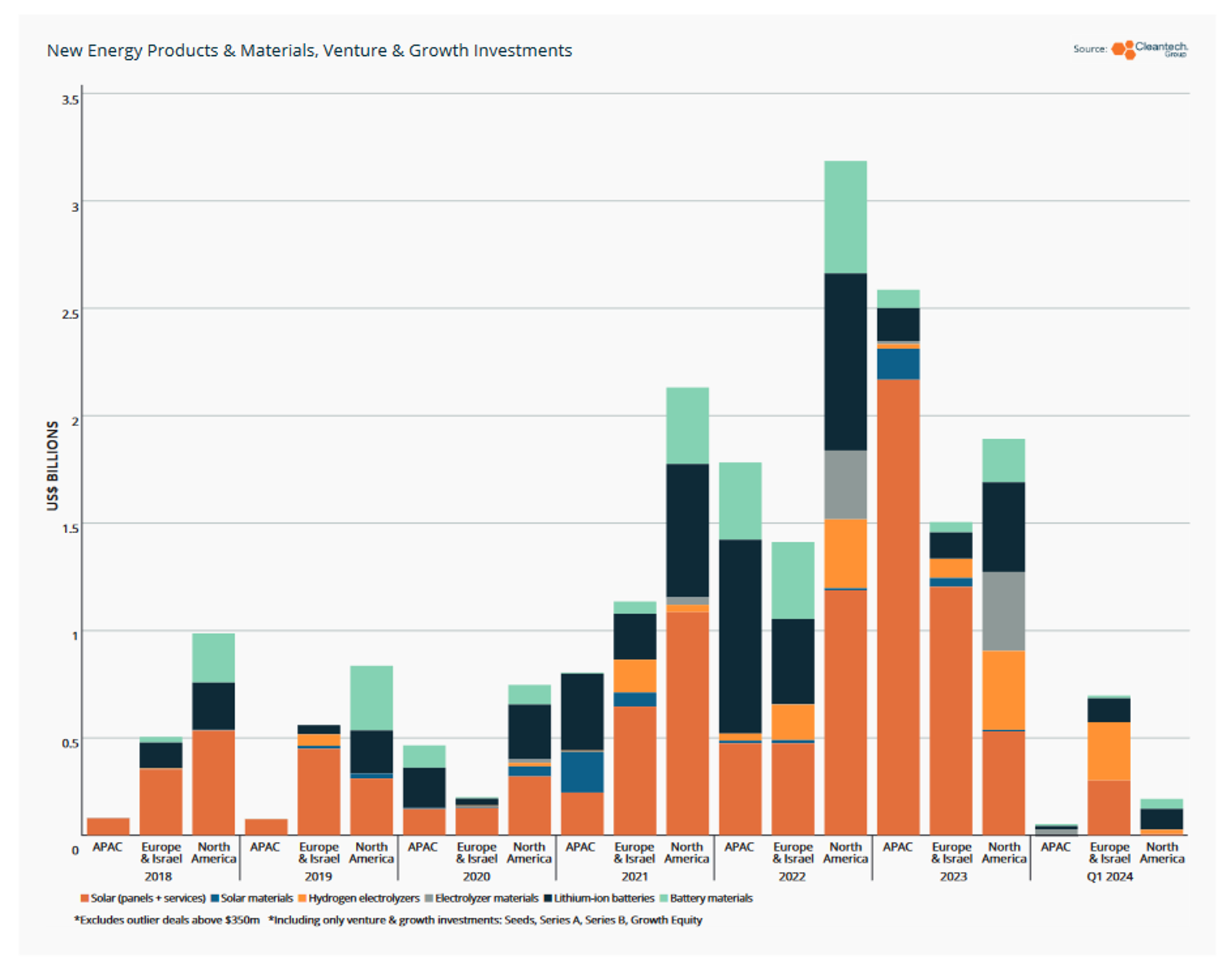

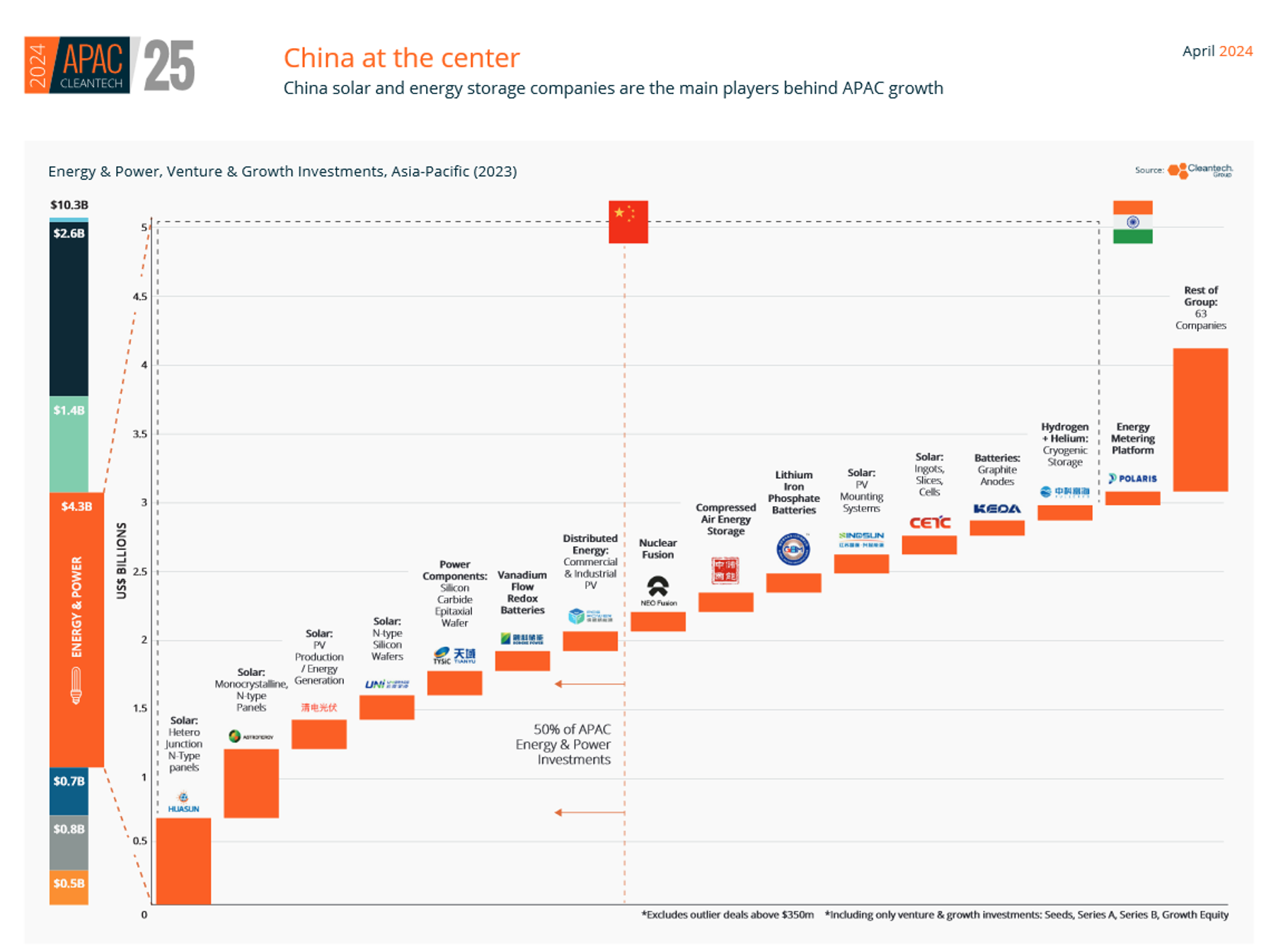

Nowhere is the “New 3” emphasis more evident than in solar – in 2023, China added around 160 gigawatts of solar capacity versus 60 gigawatts that were added in 2022. Contrast this number to the U.S., where 32 gigawatts of solar generating capacity deployed in 2023 was a record. See the “China at the Center’ graphic below, where, in terms of venture and growth investments, 4 of the top 5 most active APAC-based Energy & Power companies were all Chinese solar panel or wafer manufacturers, three of whom are producing N-type solar products. N-types are expected to comprise over half of all global output by the end of the decade.

The rapid deployment of solar in China coupled with localized supply chains have motivated more innovators to enter the storage market as well. PCG Power, a 2024 APAC Cleantech 25 company, is an example of a beneficiary of the mature solar + storage supply chain – after incorporating less than two years ago, the company is now delivering comprehensive heavy industry DER energy schemes to major manufacturers, including a new 21MW grid-connected solar installation at a Geely Automotive facility.

The APAC Materials-for-Mobility Value Chain Strengthens

Last year we noted that electric mobility in APAC was taking on geographic breadth and technology depth – with more localized vehicles, but also infrastructure innovation to smooth rollout of vehicles. This year that trend continues with more examples of localized mobility solutions in the APAC Cleantech 25 – there’s now a clear trend towards fleet electrification, as vehicle production, fleet management, and infrastructure-as-a-service models begin to converge:

- Selex (Vietnam) produces electric two-wheelers for delivery and cold chain, while also providing battery swapping subscriptions and pay-per-kilometer battery rental services.

- Newrizon (China) produces light-duty electric commercial trucks and operates a network of charging and battery swapping stations. Newrizon’s vehicles are highly digitalized with connectivity and monitoring devices to perform predictive maintenance and energy management.

- Alt Mobility (India) offers a suite of tools to support fleet managers in transitioning to electric fleets, including vehicle selection, charging planning and optimization, and predictive maintenance.

Selex Electric Bikes + Battery Swapping Stations for Delivery and Cold Chain

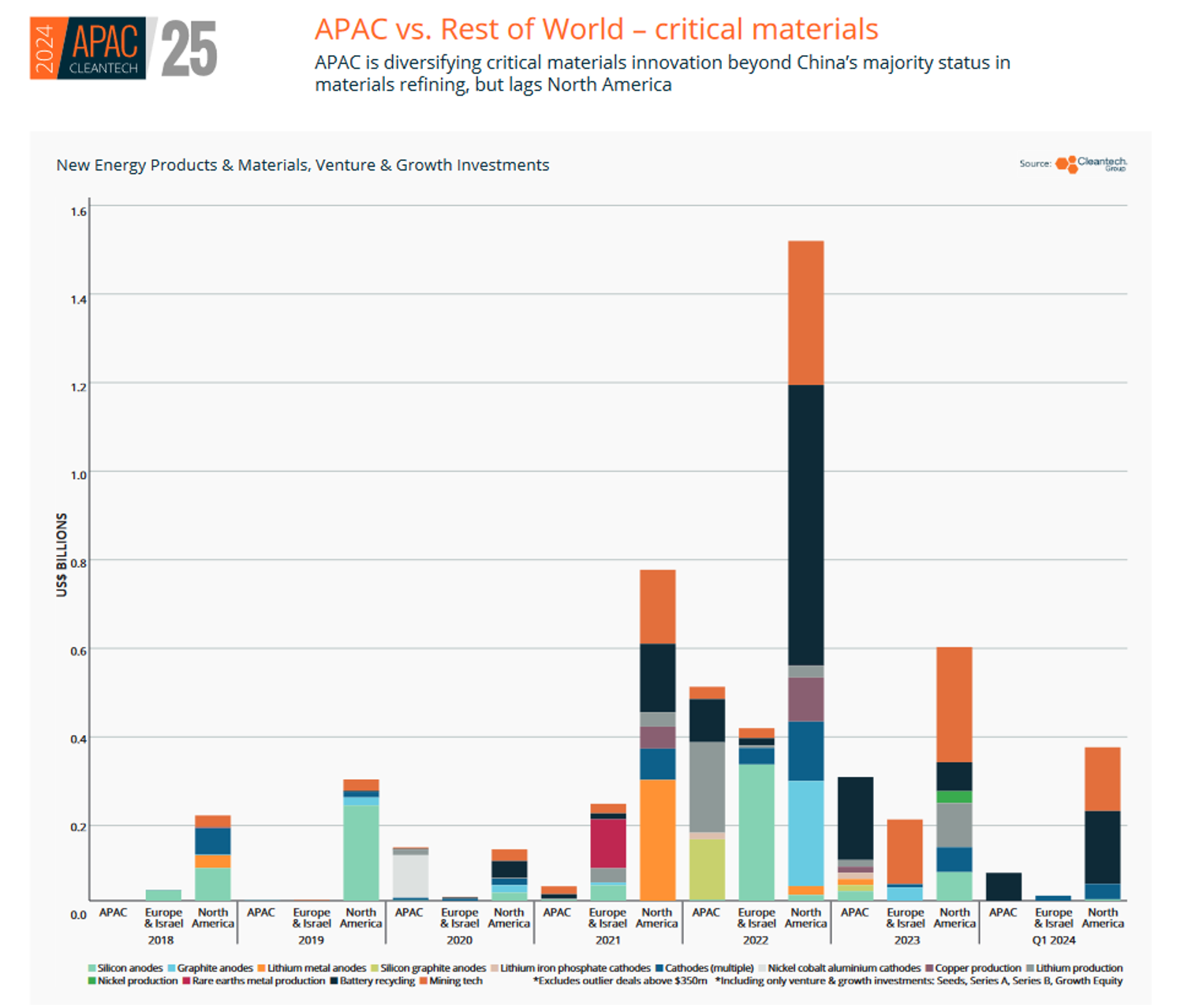

The APAC region has for years shown strength in production of finished electric vehicles and in multiple form factors (passenger vehicles, trucks, two- and three-wheelers). And while many are aware of China’s long-standing domination of battery materials supply chains, fewer are aware of the deeper innovation occurring in the region around higher-performing battery materials and resource-efficient access to raw materials. In terms of venture and growth investments in critical materials innovation, APAC has led Europe since 2022 – what is different now is that innovation is developing across the value chain but with notable progress on the furthest upstream of materials extraction and furthest downstream of battery recycling.

This year’s APAC Cleantech 25 list shows a pan-APAC effort to succeed in critical materials onshoring, but also to develop the exportable technologies that any country with an onshoring priority will want to engage:

- Novalith (Australia) uses CO2 from industrial processes to replace sulphuric acid in the lithium extraction process to produce smaller footprint lithium and flatten the carbon emissions profile of extraction.

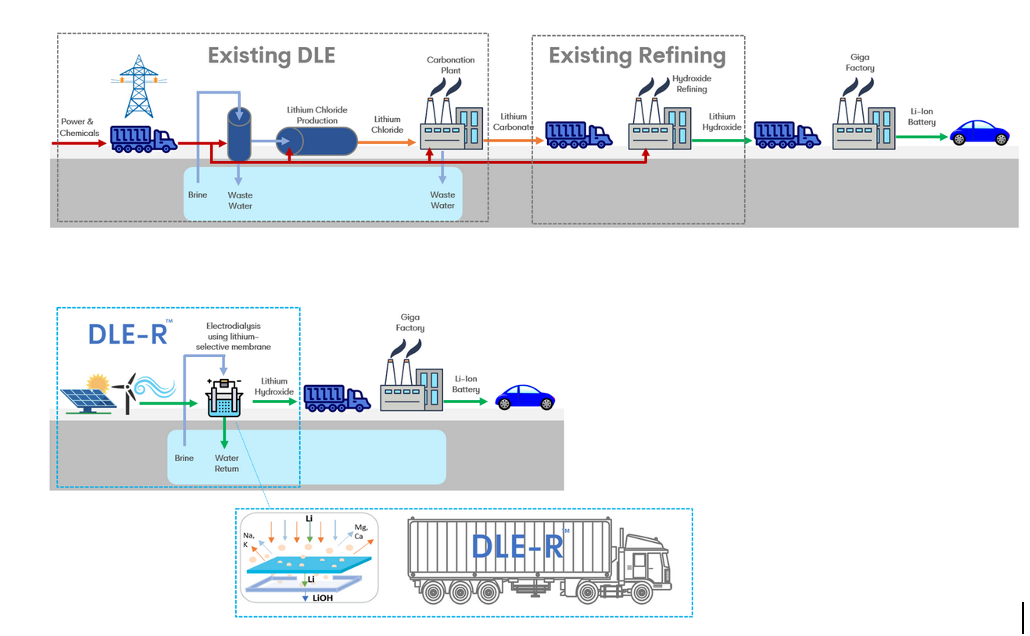

- Electralith (Australia) has further compressed the direct lithium extraction process by leveraging a proprietary membrane separation technology to extract lithium from brines and convert to lithium hydroxide in one step (versus incumbent processes that have an extra conversion step from lithium carbonate to lithium hydroxide).

- Geo40 (New Zealand) recovers silica and lithium from geothermal reservoirs, allowing for co-location with geothermal power operations.

- Sicona (Australia) has developed a silicon carbide material for batteries that has the potential to be a drop-in replacement for graphite anodes but with up to 4.5x capacity.

- Ruilong Tech (China) is recycling lithium-ion batteries at scale through 4 facilities that carry out crushing, dismantling, and hydrometallurgical processing of batteries to recover lithium, cobalt, and nickel.

Electralith’s Novel Direct Lithium Extraction and Refining Approach

APAC Innovation Nudging Industry Cleaner and Smarter

Consistent with themes we’ve seen globally, APAC innovators are capitalizing on a global need to manufacture in a cleaner but cost-effective manner. Industrial decarbonization and circularity were on full display in this year’s APAC Cleantech 25.

Enhanced weathering for carbon capture-to-value is an emerging theme, and two companies on the list demonstrate distinct approaches:

- Aspiring Materials (New Zealand) is processing olivine-rich rocks, typically dug out of the Earth as a mining byproduct, into a magnesium hydroxide that can be used in carbon capture. The resulting compound (magnesium carbonate) locks the carbon away, and can be applied in production of building materials, fertilizers, and other global industries.

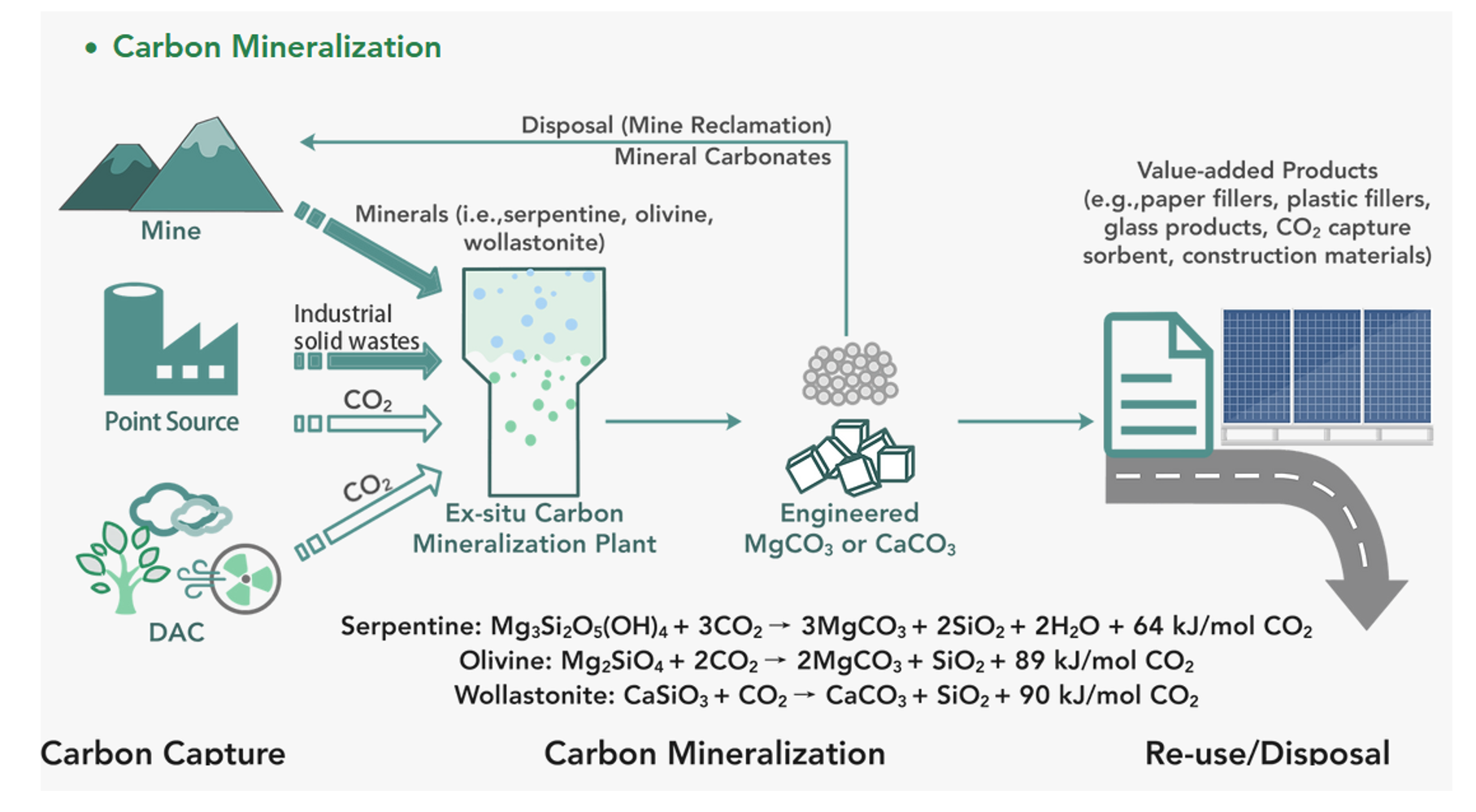

- GreenOre (China) is similarly using abundant rocks as an ingredient to the carbon mineralization process, which is already being used to process steel slag. The underlying technology can be applied across industries to take industrial slag, ash, or general mineral-dense waste to valuable products.

Others are attacking the challenges of emissions intensity in specific mineral processing. Take Zincovery (New Zealand), who has developed a hydrogen-based process for producing high-purity zinc without fossil fuels.

GreenOre’s Carbon Mineralization Process

Elsewhere, there are multiple companies taking on the challenge of plastic waste – a problem that has special relevance to Asia, where an estimated 80% of oceanic plastic waste resides.

- Samsara (Australia) is taking an ambitious approach to enzymatic recycling that allows for processing of complex polymers back down to simple monomers, functionally allowing for the creation of new virgin plastics from plastic waste.

- BluePlanet (Singapore) operates recycling businesses from cement waste to biomass and e-waste, but is also producing fuel oil from plastic waste through a Thermo-Catalytic Depolymerisation (TCD) process.

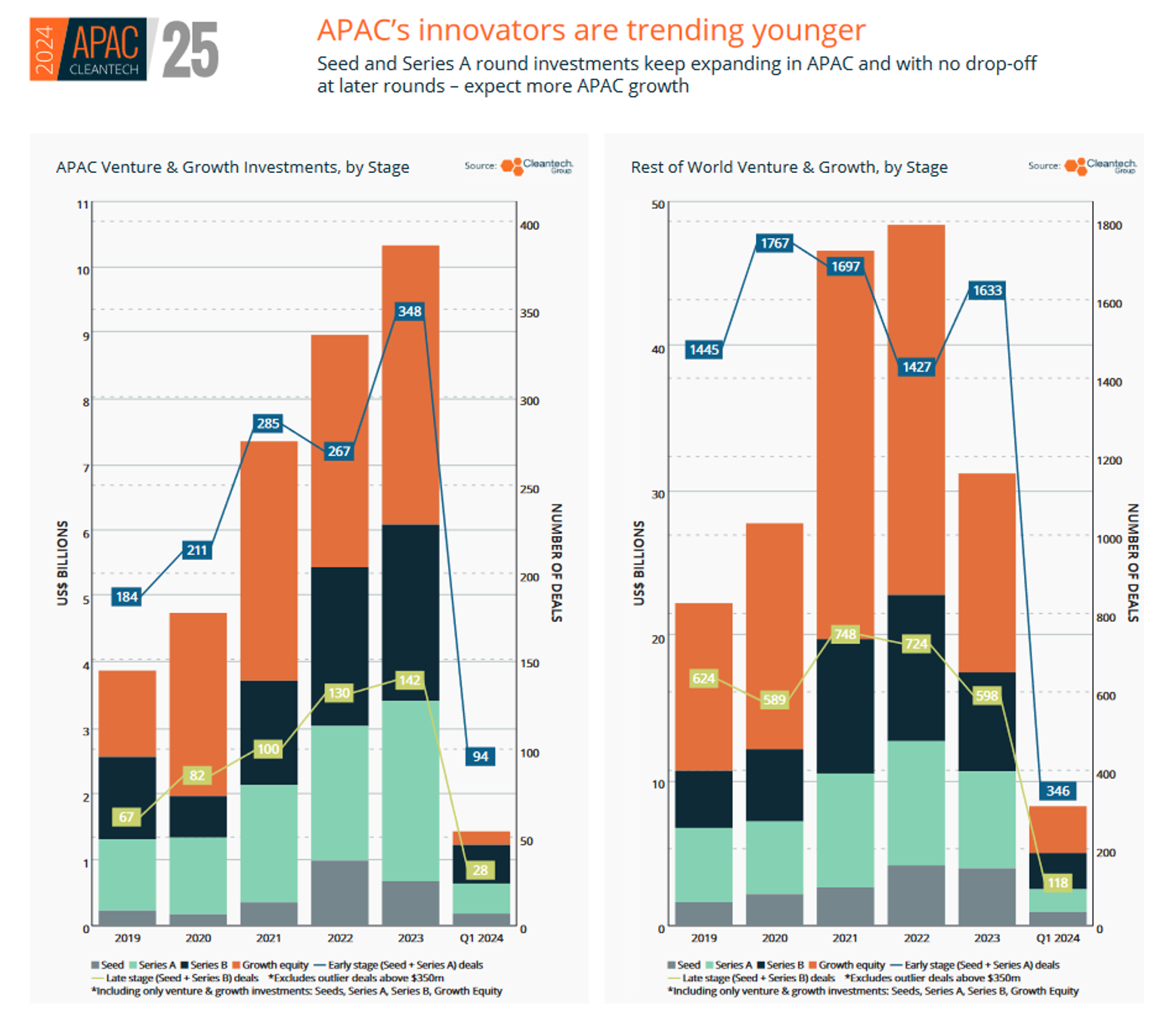

We have covered at length over the past few months a marked shift since the pandemic to a more deep tech-focused cleantech economy that is emerging. This is undeniably taking shape in APAC, and with a continued intersection of manufacturing and climate, more industry veterans than ever are transitioning into cleantech innovation. If we take the chart below, where Seed and Series A deals comprise a higher percentage of cleantech deals in APAC than the rest of the world and are rising each year, we should expect to see even more unique innovation launched out of the region in coming years.