Hydrogen Production: Can We Get to $1 Clean Hydrogen?

Last week, the European Commission opened the doors to applications for the initial phase of a regional 40GW 2030 plan, targeting the installation of 6GW of electrolyzers to produce one million tons of hydrogen, all by 2024. A day now rarely passes without an ambitious multi-gigawatt project announcement, hitting the headlines. The Hydrogen Council cited $300b billion earmarked for 228 projects this February, with strategic national targets now earmarked in 17.48% of the global GDP.

The hope is via rapid scaling through this decade, hydrogen produced using renewable electricity can be:

- Cost competitive to hydrogen produced using fossil fuels

- Help decarbonize many of the hard-to-abate sectors such as steel, cement and chemicals

- Play a major role as a seasonal storage mechanism within the power sector

Nel, one of the world largest electrolysis manufactures, announced in January a target to produce renewable hydrogen at $1.50 per kilo by 2025 (assuming an electricity cost of $20/MW). The group believes through economies of scale, standardization and system efficiency improvements, today’s more mature options (Proton Exchange Membrane (PEM) and Alkaline) can achieve the fossil fuel hydrogen cost breakpoint.

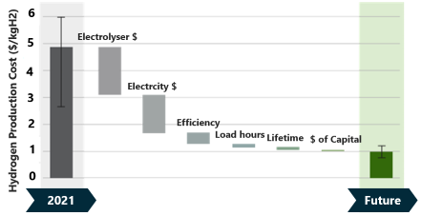

Lessons from the solar and wind industry have taught us these expansions can certainly help. However, many market spectators believe intrinsic bottlenecks surrounding the use of expensive materials, issues around acidity-induced unreliability and a large dependency on abundant, widely available renewable power, means we have not reached the “end game” when it comes to preferred technology choice for every application. The options for cost reduction are broken down in the figure below. Recognizing this need for improvements on capital costs, efficiency and renewable power costs, innovators are racing to commercialize a new wave of clean production technologies to get clean hydrogen to $1/kg as the market grows from $177 billion to $320 billion by 2030.

Figure 1 Electrolyser cost breakdown, Cleantech Group & IRENA Green Hydrogen 2020

Figure 1 Electrolyser cost breakdown, Cleantech Group & IRENA Green Hydrogen 2020

Improving renewable electrolysis

Renewable power electrolysis is at the heart of large-scale efforts. This is due in part to its relative maturity, ability to rapidly scale and enable long-term capacity planning. Beyond the scale efforts, emerging innovators are rapidly reducing capital costs through novel stack/cell design, removal of expensive materials and by substituting renewable power for recycled feedstocks including biomass and waste. Here are some of the innovators creating momentum the market:

- Building on the flexibility PEM brings, innovators including Hystar and 1s1 Energy are redesigning process architecture to reduce the electricity consumption to lower the overall cost of PEM-based production. A reduction in operating costs means PEM could become more cost competitive to large-scale alkaline electrolyser projects.

- Introducing heat as one of the feedstocks to hydrogen synthesis can drive down operational costs, in adjacent industrial facilities where process heat can be used. Innovator Sunfire has commercialized a reversible solid-oxide electrolyzer into many of the flagship industrial projects including BAT, working in ceramics and MultiPLHY, creating biofuels.

- Another cost cutting strategy is to reduce additional pressurization stages needed for many off-takers. The ammonia market for example attributes 25% of their costs towards gas compression. Ergosup uses a two-stage system to separate out hydrogen and oxygen production, producing hydrogen at high pressure. Supercritical Solutions is also using a multi-stage process to produce hydrogen at high pressure, but also is heating water to a super-critical state.

- Multi-stage hydrogen production can also reduce capital costs through the removal of expensive catalysts or other materials. Both Clean Power Hydrogen, using membrane-free, cryogenics and H2Pro, developing electro-thermochemical systems are building momentum from investors and are moving towards scaled manufacturing.

- Anion Exchange Membrane electrolysis is a hopeful technology set combining a flexible PEM-style balance of plant, but with the use of low-cost materials, similar to Alkaline. Innovator Enapter plans to the launch the first large scale AEM manufacturing facility running next year. The exact pathway for system design remains to be decided, as emerging innovators Origen Hydrogen and Versogen use alternative designs address membrane durability issues.

- Other innovators negate renewables electricity all together, and instead using biomass, biofuel or waste to drive down the costs. Gasification using biomass has been practiced for a while at large-scale, however, innovators are looking at improve on current systems through increased system modularity, standardization, or by using alternative feedstocks including paper (US-based SG H2 is building a plant in California to produce 3.8 million KG of H2 per year) or wastewater (Ways2H, who recently partnered with Japan Blue Energy to convert sewage sludge into renewable hydrogen). Such systems can be carbon neutral if the right volume of recycled feedstock is used and can benefit from waste collection tax credits.

Making low-carbon hydrogen future proof

Today’s hydrogen is anything but clean. In truth, 99% of the produced hydrogen comes from fossil fuel-based production. Many believe relying on these technologies to meet the increase in demand offers a viable alternative pathway which addresses concerns around stranded assets. The pool of solutions is classed as “Low Carbon Hydrogen Production”, tapping fossil fuels in combination with some CO2 capture to produce low-cost hydrogen.

Steam Methane Reforming (SMR) combined with point-source carbon capture technology is widely being explored globally. Many of the innovators in the space are looking to improve on a number of ranging variables including the percentage of CO2 captured, system size, and feedstock flexibility.

- ZEG Power is developing an enhanced SMR system that makes use of a calcium carbide to capture and store carbon. The company is looking to capture upwards of 70% of the CO2 and is developing a pilot plant adjacent to the Northern Lights CCUS project.

- Other steam reforming innovators including Bayotech offer on-site hydrogen production, and also the opportunity switch in biomass/waste as a feedstock where available. Bayotech has raised over $170 million in equity today, with development partners established globally.

- Similarly, other innovators see fossil fuel feedstock as a steppingstone towards a future which can rely solely on renewable feedstocks. Syzygy Plasmonics and Solistra are developing solutions which can use fossil fuels or bio gas in combination with sunlight to produce low carbon hydrogen.

- For many, the inability to fully capture carbon is an argument on why such options should be omitted from any long-term planning. To address the issue, methane pyrolysis production is emerging as popular innovation theme which offers permanent carbon-lock, producing a solid carbon block with no leakage. Innovators are introducing variations within the pyrolysis technology suite, including C-Zero, Monolith Materials and Ekona Power who are supported by strategic corporates, financially invested in prolonging natural gas markets in Canada and the US.

Winners? Losers? What really matters is use-case

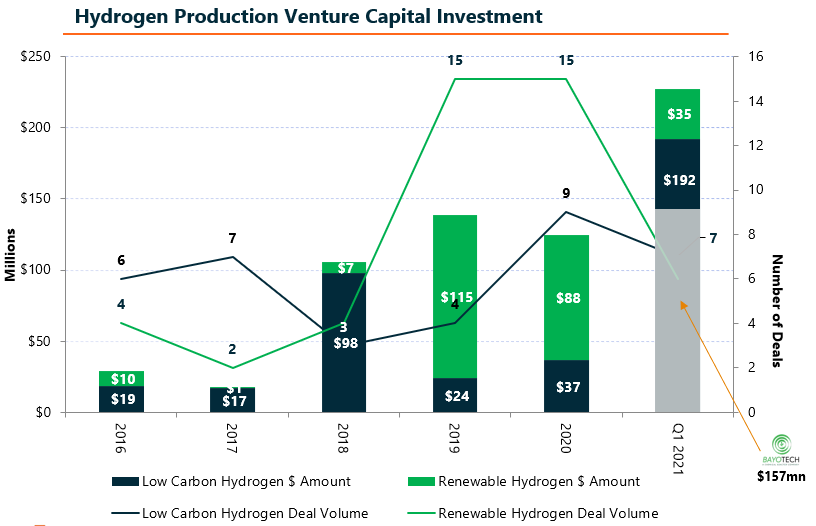

Both sides of the renewable or low-carbon markets have innovators working on solutions which promise future hydrogen costs lower which can be achieved by mature technologies, and carbon intensities lower than available today. As a result, cleantech investors are engaging with both sides, seen in the figure below. A portfolio approach is being taken given the exploratory, early-state of the market.

Figure 2 Hydrogen Production VC investment, Cleantech Group

Figure 2 Hydrogen Production VC investment, Cleantech Group

Across many countries, both sides of the renewable or low-carbon markets have innovators working on solutions which promise lower future hydrogen costs which can be achieved by mature technologies, and carbon intensities lower than available today. As a result, cleantech investors are engaging with both sides, seen in the figure below. A portfolio approach is being taken given the exploratory, early-state of the market.

- Act as a backbone to facilitate the growth of renewable hydrogen.

- Develop access to a market demand.

- Make a dent on the carbon budget this decade.

- Address the issue of stranded fossil fuels assets.

- Give time for dedicated renewable energy supply to build.

Other stakeholders believe low-carbon hydrogen may be an inhibitor to investment and growth of renewable hydrogen. At both the early and late-stage side of the markets, support is largely driven by either geographic availability of low-cost renewables or by the availability of low-cost natural gas. Policy support for renewable additionality, or ongoing public support for natural gas plays a key role globally in determining which technologies may be suitable in which locations.

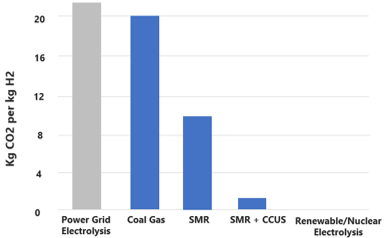

In truth, it is difficult to over emphasize the importance of either side without viewing the overall lifecycle emissions of a technology. As can been seen below, lack of supportive policy and mismatching in power grid supply and demand means that hydrogen produced using electrolysis is in fact more carbon intensive than using SMR today.

Figure 3: Hydrogen Production Lifecycle emissions, Cleantech Group

Figure 3: Hydrogen Production Lifecycle emissions, Cleantech Group

Producing hydrogen at $1 per kg cleanly will therefore require a mixture of innovation which ultimately depends on the specific requirements of the offtakers.

- Do you need hydrogen in a small volume on an intermittent basis?

- AEM electrolysis or advanced PEM electrolysis could be your route.

- Can you run an ammonia plant with fixed requirements for large-scale supply?

- Alkaline electrolysis, biowaste gasification, or enhanced SMR + CCUS could work, but the availability of gas, waste or renewables will dictate your affordability.

While lessons from the wind and solar sector have shown it’s not necessarily the best technology that wins out, it is worth noting the hydrogen market is by no means new, with corporates, governments and other stakeholders looking to ensure they maintain relevance in the potential $2.5 trillion hydrogen market, projected by 2050.

Keep an eye on

- Innovators focused less on technology development, moving downstream as project developers (HDF Energy, The Hydrogen Utility, Lhyfe), or playing in end-use markets, integrating other tech into products (Sylfen, Home Power Solutions).

- Innovators developing blockchain technology to guarantee the renewable origin of green hydrogen. FlexiDAO is running a pilot with Acciona called GreenH2chain which could help electrolyzers powered by the grid reduce overall emissions.

- Corporates working on offshore wind turbines with integrated electrolyzers. Siemens, TechnipFMC, RWE and Vattenfall are all exploring the idea to reduce the need to developing dedicated hydrogen transmission networks.