Indoor Farming: What’s Next for Greenhouses, Vertical Farms and Container Farms?

Some pioneering and high-tech indoor farming systems have struggled to meet return on investment expectations, but increasing automation, decreasing cost of capital and improving market conditions lie ahead. The indoor farming technology market was valued at $23 billion in 2016, and is projected to reach $ 40.25 billion by 2022 (with a robust CAGR of 9.65%). The current market value of crops grown in greenhouses worldwide is approximately $300 billion.

What’s Driving Indoor Farming Investment?

Indoor farming enables farmers to reduce risks associated with the weather and increase per acre productivity. It also uses fewer resources and produces more per square foot. In a world where there is decreasing availability of arable land, this is a critical farming method. As the recent World Resources Institute Report, it is estimated an area twice the size of India will be required for new agriculture by 2050 even if increasing productivity follows the strong upward trend of the last fifty years.

Consumer preferences are changing. While there is a willingness to pay for fresher and more healthy food, the biggest premiums are placed on ‘local’ food. This is a key selling point for growers who can locate in or near urban centers.

Food safety is an increasingly valuable part of vertical farming, as food-born illness is estimated to cost the US economy $15.6 billion per year. In the U.S., there have been many recent high-profile outbreaks of E. coli in Romaine lettuce due to washing practices. Vertical farms are controlled growing environments where no washing is required.

North America is a Key Market for Indoor Farming

North America is the largest market for new indoor farming technologies. Why? The region pays high prices for fresh produce, key technology such as lighting is cheap and the cost of capital is low, especially compared to other regions such as Europe.

In the U.S., costs for premium products like fresh herbs is typically higher than in European markets. Indoor farmers are therefore able to charge a premium price to grow an expensive product. e.g. in the U.S. basil is typically $5 /box whereas UK prices are >$2/box.

There is a strong pipeline of commercial scale growing facilities being developed in North America. Current projects are focused on the leafy green market with an increasing investor appetite for greenhouse solutions such as BrightFarms and Little Leaf Farms.

Labor Costs and Automation

There is evidence showing that the leading high-tech U.S. indoor growers are running farming operations with OPEX costs that leave the system unprofitable. Indeed, growers such as Plenty promised ten new farms by 2020 when they received $200 million in funding from Softbank, Bezos Expeditions, Innovation Endeavours, and others, in 2017. To date, the company has only planned to build a new farm in Los Angeles and shuttered a project in Seattle. AeroFarms promised twenty-five new farms in five years when it received $100 million from Ikea Group, Wheatsheaf Investments, ADM Capital, and others. The company broke ground on its second commercial facility in 2019. This indicates that current sunless indoor growing facilities are mostly R&D facilities that will require increased automation when they build out commercial scale facilities.

This is ushering in a wave of investment in highly automated farms. Jones Food Company is offering ‘medical grade’ growing systems with no human interaction with the product. Fifth Season’s new $35 million plant will have forty separate robot systems in operation. Intelligent Growth Systems (IGS) have pivoted their business model from licensing farming systems to selling farming systems with a proprietary software-as-a-service layer. The company sells to local growers who understand local market conditions. IGS’s expertise focuses on reducing three key costs: power, labor and capital. The company claims a 50% reduction of lighting costs (compared to alternative LED lighted environments in vertical systems), an 80% reduction of labor costs (depending on the labor market), and ‘cheap’ systems due to use of off-shelf components which drive down material and CAPEX costs.

Current market prices for 1 kg of leafy greens are around $33 for vertically-grown produce and $23 for organic produce. As vertical farms invest and employ higher levels of technology, they will be able to increase their competitive advantage by driving down costs.

Vertical, Greenhouse or Container?

Compared to traditional farming practices, it is:

• Three times more costly to grow in a greenhouse

• Five times more costly to grow in an indoor, sunless vertical farm

• Eights times more expensive to grow in a container farm

Vertical farms and greenhouses differ most significantly on growing area. On one end of the spectrum, a typical greenhouse will cost around $55/sq. ft. for growing bed space while a container farm will come in around $120/sq. ft. for the same space. As one of the key differentiators is square footage, the real question is: how close do you need to get to the consumer?

Container farming offers the lowest cost form of farming for the newcomer. No other system requires $100k (or less) and can be ready in a few months. Container farms are not attempting to be competitive with vertical and greenhouse farming methods, rather, they offer a solution that can, in the right circumstances, command a very high retail price due to traceability, freshness and marketing opportunity.

In-store farms are the wildcard. Retailers are buying these systems and customers are showing a willingness to pay. This is most clear with InFarm’s success in retail stores across Europe, including Marks & Spencer. Whether this is a cost-competitive way to grow food at scale is unclear.

Key Industry Partners

New business models are emerging in partnership with industry incumbents. There are a growing number of system developers who are choosing not to expand their staff, but instead partner with existing local growers, distributors, retailers and food-related corporates. A system developer wants to be the enabler of a farm’s success rather than its guarantor.

Food logistics services see container farms as a good solution because they are fast to setup, use a limited footprint and are the cheapest (CAPEX) option available to build growing capacity onsite. Sodexo’s recent investment in Freight Farms is as a good example. Sodexo will roll out Freight Farms’ system, called the Greenery, in on university campuses where cost per acre is often high and there is a predictable consumption pattern.

On-line retailers with large food distribution networks are looking to partner with vertical farming operations to fulfil the volume of high quality produce they require. This was a factor in Ocado’s decision to take a majority stake in Jones Food Company. This is the first time a retailer has taken a majority stake in a vertical farm developer, signaling the value of highly automated farm systems such as the one being developed by Jones Food Company.

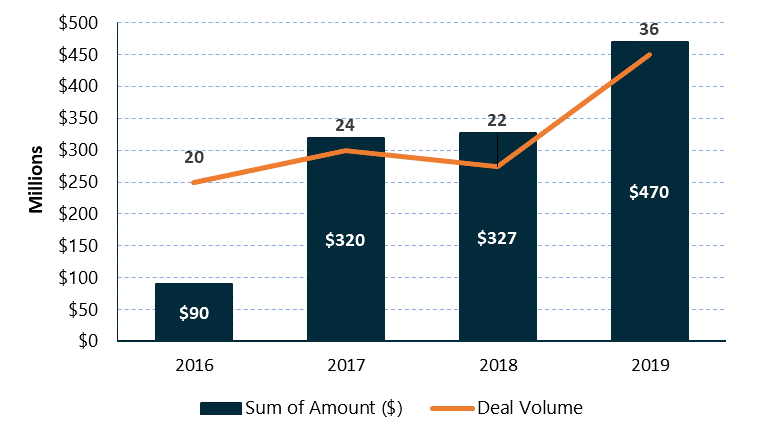

Increasing Sources of Capital are Available

In December 2019, Little Leaf Farms secured $38 million from Bank of America and doubled the size of its Massachusetts base, expanding into New York, New Jersey, Pennsylvania, and North Carolina. This is one of the first examples of automated greenhouses receiving funding from a commercial bank in the US. To add to this, private equity firms are raising funds targeting greenhouse infrastructure in the US.

Equilibrium Capital’s investment in AppHarvest and partnership with Dalsem sees the formation of a private equity backed platform for automated greenhouse farming. Equilibrium’s $336 million Controlled Environment Foods Fund, closed in April 2019, will also support the expansion of Revol Foods and Houweling Group. For these companies, Equilibrium Capital is essentially a landlord which further acknowledges the proven profitability of this growing method.

Coming up…

Chris is taking a look at innovation in the livestock value chain. Please get in touch if you would like to contribute to, and potentially feature in, upcoming insights.