Is the Wastewater Industry Striving for Better? 37 Gallons of Water for a Single Pint of Beer

In Europe, the Food and Beverage (F&B) industry accounts for 1.8% of total water use, as the industry requires large quantities of water for processing, sanitization, boiling, cooling, cleaning and as an ingredient. For example, the Water Footprint Network estimates it takes 37 gallons of water to make a single pint of beer. Meanwhile, water scarcity, regulation, increasing and changing water pollutants are making water a more critical resource for F&B corporates. So are therefore looking to innovation for cost effective solutions.

Attractiveness

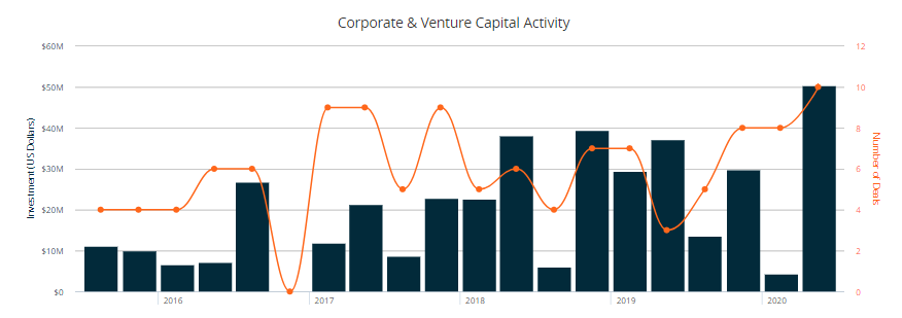

The wider industrial wastewater treatment market is estimated to be valued at $15 billion by 2024, growing at a CAGR of 5.8%. APAC is predicted to be the fastest growing market due to increasing demand from food and beverage, in addition to chemical, mining and end-use industries. We have monitored wastewater treatment over the last six years (Figure 1), the previous quarter saw both the greatest number and highest total value of investment since 2015.

Figure 1: Investment into wastewater treatment since 2015, Cleantech Group, i3 Data

Due to more stringent regulation and the rising cost of water and trade effluent discharge, traditional wastewater treatment is increasing in price, constituting a significant OpEx for commercial players. For innovators, regulation is both a driver and a challenge. The market is driven by regulation but also requires innovators to undergo long periods of R&D to prove out technologies. Regulation is less stringent in the commercial sector than municipal, so many innovators are looking to first scale and prove technologies in the commercial sector before expanding into the municipal sector with larger contract opportunities.

Business Models

Food and Beverage (F&B) wastewater is characterized by high-organic content, which is usually treated biologically. Innovation in this space focuses primarily on:

- Reducing the use of costly chemicals

- Waste-to-value business models via water and resource recovery

- Reducing energy use via energy production or efficiency gains

Due to strict punitive regulations, F&B corporates are reluctant to try new innovations. Therefore, some companies are taking a results-oriented approach by offering as-a-service business models. For example, Cambrian Innovation , developer of an onsite wastewater treatment system which recycles water and generates clean energy, offers its EcoVolt system via a Water-Energy Purchase Agreement. This offer enables wastewater treatment and resource recovery as a service.

Modularity is also a key enabler in the commercial market due to many reasons:

- In Europe, 99% of all F&B companies are SMEs, making the industry fragmented and limiting innovators’ ability to scale as SMEs cannot afford significant infrastructure or to take a risk on new innovations.

- F&B corporates have likely invested significant CapEx into existing treatment infrastructure. Innovators who can offer lower cost, modular systems to supplement and optimise existing infrastructure are able to scale faster.

- Outputs in F&B production fluctuate in concentration and pollution type, modular systems provide affordable flexibility.

We spoke to Orianna Bretschger, CEO of Aquacycl, developer of modular bioelectrochemical water treatment systems for wastewater with high carbon content. Orianna explained, “Commercially, we act as a pre-treatment so we fall under existing regulatory permits that tie to sewer. This reduces the regulatory delays and risk aversion… We can also optimize existing treatment systems, avoiding any downtime for installing a new system, while helping companies save money on an issue that is only getting worse.”

Similarly, Ekogea, developer of anaerobic waste-to-water treatment solutions for the food and beverage industries, boast lower CapEx and OpEx as well as a carbon and nutrient neutral modular systems.

Different F&B sectors vary in output, and therefore wastewater treatment solutions are being developed for specific industries. For example, brewery wastewater is particularly high in organic content, while the process is wasteful in water. Cambrian Innovation’s Ecovolt system is targeted at Breweries due to its energy positive system’s ability to recycle water and efficiently treat high organic content. Similarly, Aquacycl are gaining most traction in F&B as its bioelectrical treatment system can cheaply treat water with high organic content.

Recent Deals

- February 2020: Baswood, provider of biological wastewater treatment and biosolids/sludge management, was acquired by Cambrian Innovation. Together the companies provide a full suite of next-generation biological treatment capabilities. For Cambrian Innovation, the acquisition meets its vision to treat industry as an ecosystem — extracting resources, like clean energy and clean water, from wastewater.

- October 2019: Cambrian Innovation raised $18 million in a Growth Equity round led by energy and natural resource focussed VC investor, Spring Lake Capital. The funding was for the expansion into new market verticals and the acceleration of its service-based offering, the WEPA (Water-Energy Purchase Agreement)

- September 2019: Aquacycl closed $4 million in a seed round, The Roddenberry Foundation led the round with participation from Tech Coast Angels, Next Wave Impact, the Chemical Angel Network and other impact funds and individual angel investors.

- June 2019: Ekogea, developer of anaerobic waste-to-water treatment solutions for the food and beverage industries, was selected to join seven other start-ups in the Imagine H2O‘s Asia Accelerator for innovators reimagining a water-secure future for Southeast Asia.

Competition

There are several leading global players in the industrial wastewater treatment space, including Suez, Ecolab and Kurita Water Industries. Due to such strong incumbents, there is significant M&A activity in this market.

Orianna Bretschger, CEO of Aquacycl explained the competitive landscape, “There is lots of competition in this space, particularly in the beer and wine sectors. The commercial industry is also collaborative…what may start out as a competitive relationship could lead to paired technologies. However, the biggest competition is no engagement in innovation, the industry is highly risk adverse and for good reason – regulation is strict and companies want to avoid any downtime.”

Corporates are increasingly engaged in innovation to facilitate cost reductions and efficiency gains, while also achieving sustainability, e.g. AB InBev’s 100+ Accelerator. Large FMCGs are leading internal change via consortiums for sustainability, such as Pepsi Co’s Casa Grande, an Arizona facility that saved $80 million by reducing water use by 26% with actions focused on recycling water via biological treatment.

To look out for…

Advanced nature-based solutions for commercial wastewater treatment are gaining market traction. For example, in June 2020 Leap Frog Design, developer of greywater treatment system using plants and natural materials, was selected to join the Cascadia CleanTech Accelerator, a virtual 15-week program available to early-stage companies.

These Green Infrastructure Systems can take up less space, can be cited within cities, are more attractive than grey infrastructure, while creating green spaces for people and habitats for animals.