Soil Mapping Technologies: Regenerative Agriculture, Soil Carbon Sequestration and Ecosystem Service Payments

A key takeaway from our work on Soil Carbon, a part of the Cleantech for Europe project we are developing alongside Breakthrough Energy, was the increasing importance of understanding soil. Measurements of soil health, soil’s ability to support life and provide services like water purification, carbon sequestration and others, have always been valuable to farmers but are becoming increasingly important. In this recent research, we look at soil measurement that go beyond conventional agronomics of nitrogen, phosphorous, potassium, water, salinity, temperature, which all contribute to good soil management, and into growth areas such as carbon and microbial activity measurement.

Drivers

Driving this trend is global soil degradation due to intensive farming techniques and climate change increasing stress on crops and soils. To help combat this, innovators are finding ways to measure and price activities contributing to soil health. This is currently under-valued in price of quality crops well maintained soil creates, and as a result, direct measurements of healthy soil signals are being taken. This includes soil organic carbon (SOC) content and improved understanding of microbial activity which generate productive soils.

SOC measurements are unlocking carbon capture and sequestration payments for farmers. This is a win-win for farmers who will generate revenue for maintaining healthy soils and it can provide a significant carbon removal engine to help address climate change. Measurements of microbial activity in the soil are increasing understanding of nutrient cycling within the soil, but it is also offering developers of biological soil inputs the ability to discover new microbes (typically less than 10% of soil microbes are currently understood) but also track the impact and effectiveness of existing products to improve their ability to replace conventional agricultural chemicals.

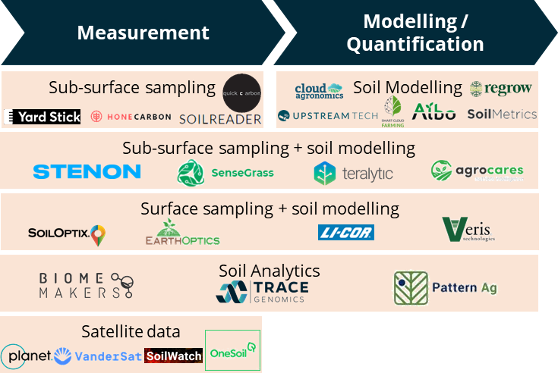

SOC measurements at scale

Some combination of physical soil sampling, remote monitoring, and soil modelling will be required to map soils’ carbon content consistently and at scale. Currently, physical sampling is too expensive to repeat at the scale required. On the other end of the spectrum, remote measurements from drones and satellites are not enough to give an accurate understanding of what is happening at depth in soils. In the middle sits modelling techniques, which help to reduce the amount of physical sampling that needs to occur and ‘ground-truth’ satellite measurements with what is observed in sub-surface sampling. Some combination of these three will provide a scalable platform to measuring SOC at scale, and at a price making sequestration payments to farmers a viable business model.

Competition

Agricultural incumbents are interested in furthering soil mapping, measuring, and monitoring technologies to improve their understanding of soil and provide better feedback into their product development cycles. This is partly why Monsanto bought Climate Corporation in 2013 at a peak of the precision agtech acquisition trend then carried through to May 2021 when Valmont Industries paid $300 million for Prospera. In the soil mapping for soil carbon sequestration industry the pool of interested corporates is wider as high-emission companies look to own, or have preferential purchase options, on sources of carbon removal and offsets. This explains why Bayer, Cargill, and Danone, all have regenerative agriculture and soil carbon sequestration support programs, but also why Microsoft purchased $2 million of soil-based carbon sequestration credits though Land O’Lakes subsidiary Truterra, and why Shell acquired carbon farming company Select Carbon in May 2020.

There is lots of regulatory work to do

While soil mapping has enough high-value applications to see significant development and investment, the carbon part of this industry is still early stage. Regulatory structures are still unclear, with private soil carbon markets creating their own protocols to measure and sell carbon, creating a fragmented patchwork of solutions with varying degrees of reliability. Governments are putting together structures for this market:

- Australia created the first soil carbon measurement methodology in 2014 to pay farmers for behavior changes,

- EU is promoting Soil Health as a key metric in its Biodiversity and Field-to-Fork Strategies,

- US government outlining the MRV framework for the agricultural Carbon Bank,

- UK Environmental Land Management Schemes (ELMS) and Agriculture Bill incentive schemes and methodology for measuring ecosystem services.

We expect to see more details about these structures towards the end of this year.

Keep an eye on…

Incumbents sit on a lot of soil data already and the potential platform play from either a corporate or a private equity firm. On the first, signals such as the partnership between Biome Makers and Bayer indicate incumbents may have the library of soil data required to build the models that can accelerate the trend towards low cost sub-surface soil mapping at scale. On the second platform strategy, Indigo acquiring Tellus Labs in 2018 is one signal of the role of remote monitoring in agriculture before announcing the Terraton Initiative in 2019. With many physical sampling, soil modelling, and remote monitoring startups out there a platform play seems likely.